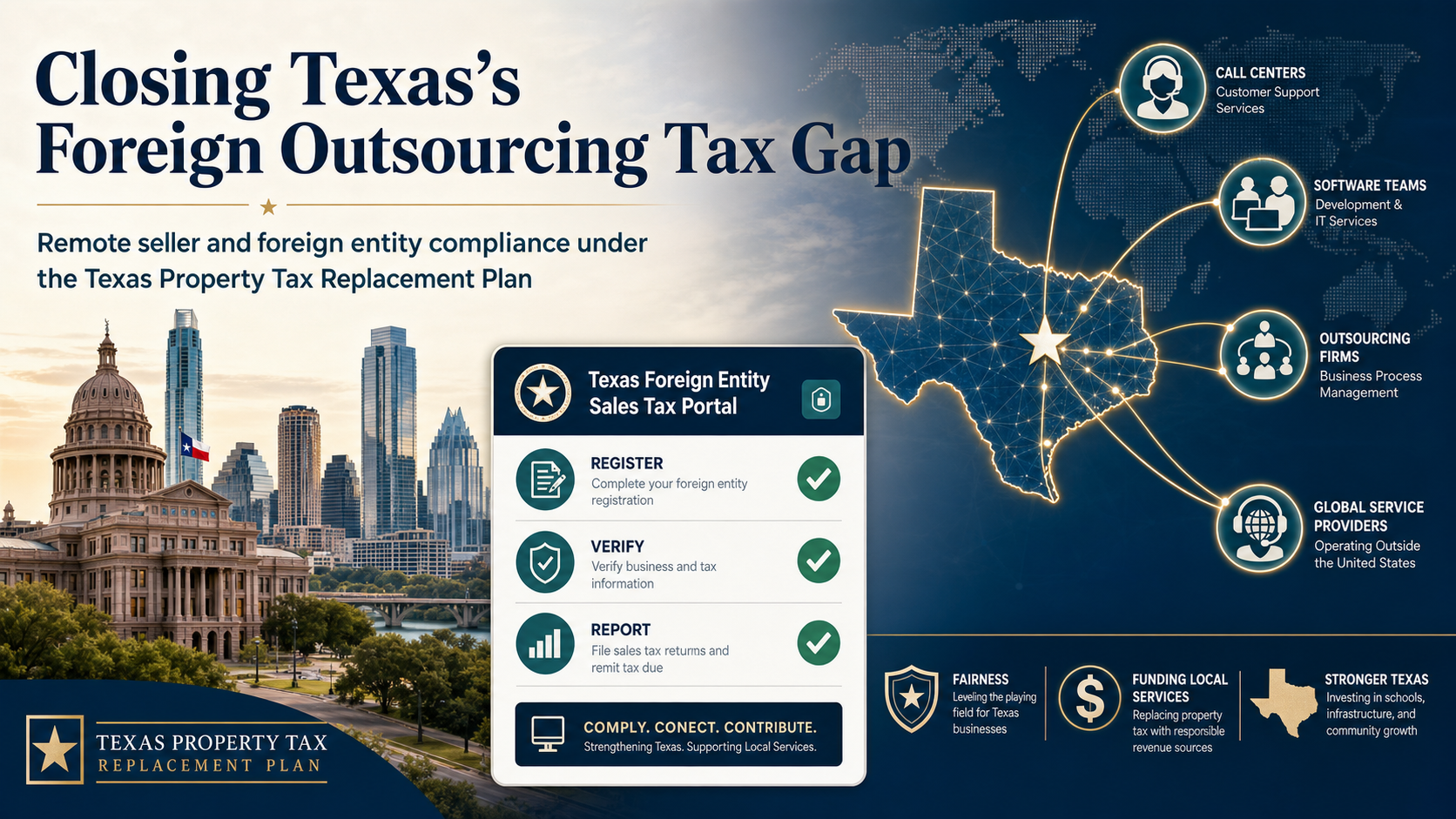

Taxing the Invisible Transaction — TPTRP Foreign Entity Sales Tax Framework

Rep. Will Campbell · House District 109 · June 23, 2026 · Texas Property Tax Replacement Plan — Working Paper

Taxing the Invisible Transaction — TPTRP Foreign Entity Sales Tax Framework

How the Texas Property Tax Replacement Plan will capture sales tax from foreign and out-of-state businesses — and why it is constitutionally sound, legally proven, and essential to a fair and complete Texas tax base.

The Invisible Gap in Texas’s Tax Base

Why foreign and out-of-state service providers represent the largest uncaptured commercial transaction category in Texas today — and why fixing it matters

Every day, Texas businesses write checks and wire payments to companies that will never set foot in this state. The call center in the Philippines handling your company’s customer support. The software development team in Bangalore building your enterprise application. The accounting firm in New York processing your accounts payable. The HR outsourcing company in Dublin managing your benefits enrollment. These are real commercial transactions — real money flowing from Texas businesses to service providers — and under the current system, not a dollar of Texas sales tax is collected on any of them.

The Texas Property Tax Replacement Plan (TPTRP) is built on a foundational principle: every commercial transaction that occurs in Texas should be part of the tax base. When a Texas business purchases a service, whether from a company down the street in Cedar Hill or from a vendor in Chennai, that transaction is occurring in Texas. The service is being consumed here, it benefits an operation here, and it is part of the economic activity that Texas’s infrastructure, legal system, and commercial environment makes possible. The current system taxes the Cedar Hill vendor and ignores the Chennai vendor. That is not a level playing field, and it is not a complete tax base.

The Core Inequity

Texas-based service providers collect and remit sales tax on every taxable transaction they deliver to Texas customers. Foreign competitors delivering identical services to the same Texas customers pay nothing — creating both a revenue gap and a structural competitive disadvantage for Texas businesses relative to foreign providers who bear no equivalent tax burden.

This article explains how the TPTRP will close that gap: the legal authority Texas already has, the constitutional framework that governs how this can be done, the international models that have proven it works at scale, and the specific legislation we will draft to implement it here. We also address the most immediate concern legislators and businesses raise: does requiring foreign companies to collect a Texas sales tax conflict with the federal government’s exclusive authority over import tariffs? The answer — grounded in settled Supreme Court precedent and the fundamental distinction between goods and services — is no.

This is not a new idea or an untested legal strategy. More than 110 countries around the world already require foreign service providers to register and collect a consumption tax when they sell services to customers within their borders. The European Union perfected the administrative mechanism for doing this more than a decade ago. The U.S. Supreme Court cleared the legal path for states in 2018 with South Dakota v. Wayfair, Inc. The only question remaining is whether Texas will act.

The Three Groups This Covers

The TPTRP foreign entity framework applies equally to three overlapping groups, all subject to the same rules:

- Foreign businesses (non-U.S. companies) providing services to Texas customers from locations outside the United States — IT outsourcing firms, BPO providers, call centers, software developers, data processors, and professional service firms domiciled in any foreign country.

- Out-of-state U.S. companies in other states providing taxable services to Texas customers remotely — the same economic nexus standard that already applies to remote goods sellers applies equally to remote service sellers.

- Digital platform intermediaries that facilitate connections between Texas businesses and foreign or out-of-state service providers — these platforms will be treated as marketplace facilitators and required to collect and remit on behalf of their vendors, capturing the long tail of providers who fall individually below the $100,000 TPTRP threshold.

Why Current Enforcement Is Inadequate

Texas already has a theoretical mechanism for addressing this gap: the use tax. When a seller fails to collect Texas sales tax, the Texas buyer is legally obligated to self-assess and remit use tax to the Comptroller. In practice, this mechanism is chronically undercollected for B2B transactions involving foreign service providers. Most Texas businesses are unaware of the obligation, and the Comptroller has no systematic way to identify and audit payments to foreign vendors who have not registered. The TPTRP replaces this passive backstop with a three-wall enforcement structure. The first wall requires the foreign or out-of-state seller to register and collect — or be legally barred from operating in the Texas market. The second wall prohibits any Texas business from transacting with an unregistered foreign or out-of-state seller when tax should be collected, attaching civil and criminal liability directly to the Texas buyer who knowingly circumvents that requirement. The third wall makes registration status publicly visible through a searchable Comptroller registry so any Texas buyer can verify compliance before transacting. Together these three mechanisms close the gap that the use tax alone cannot close.

For Foreign Businesses Reading This

If your company provides services to Texas businesses or consumers and your annual Texas revenue exceeds $500,000 under current Texas law (or will exceed $100,000 under the TPTRP framework once enacted), you are required to register with the Texas Comptroller and collect Texas sales tax on taxable services. The TPTRP will expand the taxable service categories and create a simplified online portal designed specifically for entities operating outside the U.S. Early voluntary compliance protects you from historical back-tax liability — and note that the statute of limitations does not run while you are unregistered, so delay does not reduce your exposure. A Voluntary Disclosure Program is available to make this transition orderly and cost-effective. Under the implementing legislation, Texas businesses that knowingly continue to use unregistered foreign vendors face civil and criminal consequences, which means your Texas customers will have their own legal incentive to require your compliance before continuing to work with you.

The Legal Authority Texas Already Has

South Dakota v. Wayfair, economic nexus, and why foreign entities are not exempt from Texas sales tax

Before discussing what new legislation the TPTRP needs to enact, it is important to understand what Texas law already says — because the foundation for taxing foreign and out-of-state service providers is far more solid than most people realize. The Supreme Court settled the core legal question in 2018, and Texas has been operating under the resulting framework since 2019.

The Old Rule and Why It Failed

For decades, states were prohibited from requiring companies to collect sales tax unless those companies had a physical presence in the state — an office, a warehouse, employees on the ground. That rule originated in the 1967 Supreme Court case National Bellas Hess v. Dep’t of Revenue of Illinois and was reaffirmed in 1992’s Quill Corp. v. North Dakota. As the internet economy grew, this rule created a massive loophole: online retailers and service providers with no physical presence in a state could sell billions of dollars of goods and services to that state’s residents and businesses and collect no sales tax. The physical presence rule was designed for a brick-and-mortar world, and by 2018, it had become indefensible.

South Dakota v. Wayfair, Inc. (2018)

On June 21, 2018, the Supreme Court reversed course in a 5-4 decision in South Dakota v. Wayfair, Inc. The Court held that states can require remote sellers to collect and remit sales tax based solely on economic presence — the volume of sales into the state — regardless of whether the seller has any physical presence there. The Court found that the old physical presence rule was “unsound and incorrect” in the modern digital economy and overruled both Quill and National Bellas Hess.

“The physical presence rule is not a necessary interpretation of the requirement that a state tax must be applied to an activity with a substantial nexus with the taxing State. Quill’s physical presence rule is unsound and incorrect.”Justice Kennedy, South Dakota v. Wayfair, Inc., 585 U.S. ___ (2018)

The Wayfair decision did not create a new legal right for states to tax out-of-state sellers. It removed an artificial judge-made barrier that had prevented states from enforcing a tax obligation that had existed on paper for decades. The fundamental principle — that commercial activity occurring in Texas generates a Texas tax obligation — was always correct. Wayfair simply restored the ability to enforce it against remote sellers.

Texas’s Economic Nexus Standard

Under current Texas law, economic nexus took effect in 2019 and uses a $500,000 receipts-only threshold with no separate transaction-count trigger. That is the current baseline remote-seller rule. Under the TPTRP constitutional amendment and implementing legislation, that standard is changed to a $100,000 Texas-receipts economic nexus floor so that out-of-state and foreign sellers with meaningful Texas market activity are brought into the collection obligation earlier and more consistently with the post-Wayfair approach used in many states.

Texas Economic Nexus vs. Selected States

Dollar and transaction thresholds that trigger mandatory sales tax collection for remote sellers — domestic or foreign

| State | Dollar Threshold | Transaction Threshold | Effective Date |

|---|---|---|---|

| Texas | $500,000 | None (dollar-only) | Oct. 1, 2019 |

| South Dakota (Wayfair plaintiff) | $100,000 | 200 transactions | Jan. 1, 2019 |

| California | $500,000 | None | Apr. 1, 2019 |

| New York | $500,000 | 100 transactions | Jun. 21, 2018 |

| Florida | $100,000 | None | Jul. 1, 2021 |

| Washington | $100,000 | None | Oct. 1, 2018 |

| TPTRP (all commercial services) | $100,000 | None (dollar-only) | Upon enactment |

Foreign Entities Are Not Exempt

The point that surprises many people — and that is important to establish clearly for foreign businesses reading this — is that the Wayfair economic nexus framework applies equally to foreign (non-U.S.) companies. The Texas Comptroller’s economic nexus rules contain no foreign company exemption. Non-resident suppliers of services are required to collect and remit sales tax in the same manner as U.S.-based counterparts once they exceed the $500,000 threshold.

And for foreign entities that believe they are shielded by international tax agreements: federal income tax treaties between the United States and foreign countries do not apply to state sales taxes. States are not parties to these treaties. Even if a foreign company is completely exempt from U.S. federal income tax under a treaty because it lacks a “permanent establishment” in the United States, it is still fully subject to Texas sales and use tax — under current Texas law once it meets the $500,000 threshold, and under the TPTRP framework once it exceeds $100,000 in Texas receipts. These are two entirely separate legal regimes, and treaty protections from one do not carry over to the other. Multiple national accounting firms specializing in U.S. state tax compliance have confirmed this point explicitly.

For Legislators: The Key Point on Legal Authority

Texas does not need new constitutional authority or novel legal theory to tax foreign entities doing business here. That authority already exists under Wayfair and Texas’s implemented economic nexus rules. What the TPTRP needs is: (1) legislative expansion of the taxable services base to cover all commercial service transactions; and (2) a simplified registration and remittance mechanism that makes compliance practical for entities operating outside the United States. The legislation we draft in this article accomplishes both.

The Constitutional Framework

Complete Auto Transit, the Foreign Commerce Clause, the Import-Export Clause, and the Due Process Clause — what the Constitution actually requires for the TPTRP to be legally sound

Any state tax on commerce must satisfy constitutional requirements. For the TPTRP’s foreign entity collection mechanism, three constitutional provisions are relevant: the Commerce Clause (including its foreign commerce dimensions), the Import-Export Clause, and the Due Process Clause. All three have been extensively litigated, and the law is settled and favorable to what the TPTRP proposes — provided the legislation is designed correctly. This section explains the specific requirements and how the TPTRP satisfies each.

The Complete Auto Transit Four-Prong Test

Since 1977, the Supreme Court has applied a four-part test from Complete Auto Transit, Inc. v. Brady (430 U.S. 274) to evaluate whether a state tax on commerce is constitutional under the Commerce Clause. Every state tax on interstate or international commerce must satisfy all four prongs:

The Complete Auto Transit Test — Applied to the TPTRP Foreign Entity Mechanism

All state taxes on interstate or international commerce must satisfy each prong; foreign commerce adds two additional requirements

| Prong | Constitutional Requirement | How the TPTRP Satisfies It |

|---|---|---|

| 1 — Substantial Nexus | Tax must apply to activity with a substantial connection to the taxing state | $500,000 in Texas revenue establishes clear economic nexus as confirmed by Wayfair (2018) |

| 2 — Fair Apportionment | Tax must be fairly apportioned to prevent double taxation across jurisdictions | Only the portion of a service used in Texas is taxable; multi-state allocation rules codified in legislation |

| 3 — Non-Discrimination | Tax must not discriminate against interstate or foreign commerce | Identical rate and rules apply to all sellers regardless of state or country of origin; no discriminatory surcharge |

| 4 — Fair Relation to State Services | Tax must fairly relate to services the state provides to the taxpayer | Texas market access, legal system, infrastructure, and commercial ecosystem directly benefit all sellers doing business here |

| 5 — No Enhanced Multiple Taxation Risk* | Must not create greater double taxation risk for foreign entities than for domestic ones | Apportionment rules and inter-jurisdictional credit provisions prevent unconstitutional double taxation |

| 6 — Federal “One Voice” Doctrine* | Must not prevent the federal government from speaking with one voice in regulating foreign commercial relations | Universal, non-discriminatory application; no country-specific targeting; treaty monitoring provision in legislation |

The Import-Export Clause: Why It Does Not Apply to Services

The single most common objection raised to requiring foreign service providers to collect a Texas sales tax is the Import-Export Clause of the U.S. Constitution (Article I, Section 10, Clause 2). The Clause prohibits states from imposing taxes on imports and exports — a power reserved exclusively to the federal government and exercised through the customs and tariff system. This is a legitimate constitutional provision to take seriously. And it has a clear, legally settled answer.

The Critical Distinction: Goods vs. Services

The Import-Export Clause has been consistently interpreted by the Supreme Court — beginning with Woodruff v. Parham (1869) and followed through modern case law — to apply only to goods (tangible personal property) imported from or exported to foreign countries. It does not extend to services. Since the outsourcing transactions at issue in the TPTRP — IT services, data processing, call center operations, BPO, consulting, staffing, professional services — are all services, not imported goods, the Import-Export Clause creates no constitutional barrier whatsoever. Cornell Law School’s constitutional analysis and the Library of Congress’s Congressional Research Service both confirm this interpretation.

When Texas requires a software development firm in India to collect and remit Texas sales tax on development services delivered to a Texas client, Texas is not imposing an import tariff on imported goods. It is applying a consumption tax to a commercial service transaction that was consumed in Texas. The federal government’s exclusive customs and tariff authority — which applies to goods crossing the U.S. border — is completely untouched. These are different types of transactions subject to different constitutional frameworks, and the distinction is clear and settled in the law.

The “Speaks With One Voice” Doctrine

The second Foreign Commerce Clause consideration — and the most legally nuanced — is the principle that state actions must not interfere with the federal government’s capacity to manage foreign commercial relations. This “speaks with one voice” doctrine could theoretically be invoked against a Texas law that targeted foreign service providers specifically or treated them differently from domestic providers.

The Supreme Court’s 1994 decision in Barclays Bank PLC v. Franchise Tax Board of California is directly controlling here. The Court held that a state tax does not violate the “speaks with one voice” doctrine absent an actual congressional directive prohibiting the state action. Executive branch objections, foreign government complaints, and diplomatic discomfort are not enough — Congress must act affirmatively to preempt the state. A non-discriminatory, generally applicable sales tax on services delivered to Texas consumers — applied at the same rate as services from domestic Texas providers — does not impede federal foreign policy and is constitutionally sound under Barclays.

Constitutional Design Rule: Non-Discrimination Is Everything

The single most important design principle for the TPTRP foreign entity tax is that it must apply the same rate and the same rules to all remote sellers regardless of national origin. No country-specific treatment. No foreign surcharges. No different compliance requirements for entities from particular countries. Identical application of Texas’s universal sales tax to all commercial transactions in Texas, regardless of where the seller is located. This is the key to satisfying all six constitutional prongs. Any departure from this principle — even if politically motivated by concerns about specific countries — would create serious constitutional risk.

Due Process: Minimum Contacts

The Due Process Clause requires that a seller have “minimum contacts” with a state before that state can impose tax obligations. Post-Wayfair, $100,000 in annual Texas revenue under the TPTRP framework — representing a sustained, deliberate, and substantial commercial relationship with Texas customers — far exceeds any reasonable minimum contacts threshold. The due process consideration does not create a meaningful barrier for the TPTRP.

Texas Taxable Services: What’s In, What’s Missing

The current 17-category framework under Tax Code § 151.0101, the gaps in coverage for outsourcing transactions, and the legislative expansion the TPTRP requires

Texas Tax Code Section 151.0101 defines 17 broad categories of “taxable services” subject to the 6.25% state sales and use tax. Some of these categories already capture certain outsourcing transactions. Others leave the highest-volume outsourcing categories entirely outside the tax base. Understanding the current framework and its gaps is essential to drafting the TPTRP legislation correctly, because the foreign entity collection mechanism is only as effective as the taxable service base it operates on.

Texas Taxable Services — Outsourcing Relevance Assessment

Current taxability status of major outsourcing service categories under Texas Tax Code § 151.0101 (2025)

| Service Category | Outsourcing Relevance | Current TX Status | Common Foreign Outsourcing Examples |

|---|---|---|---|

| Data Processing Services | Very High | Taxable (80% of charge) | Payroll processing, data entry, cloud hosting, SaaS applications, accounts payable/receivable automation |

| Information Services | High | Taxable (80% of charge) | Database subscriptions, financial data services, research services, market intelligence, mailing lists |

| Telecommunications Services | High | Taxable (100%) | VoIP platforms, data transmission, business communications infrastructure |

| Credit Reporting Services | Moderate | Taxable (if debtor in TX) | Third-party credit bureau services, background checks |

| Debt Collection Services | Moderate | Taxable (if debtor in TX) | Offshore debt collection centers operating for Texas creditors |

| Security Services | Moderate | Taxable | Cybersecurity monitoring, digital forensic services |

| Insurance Services | Moderate | Taxable | Claims processing, actuarial analysis, underwriting support |

| Professional Services (legal, accounting, consulting, engineering) | Very High | NOT taxable | Law firms, CPA firms, management consulting, engineering, financial advisory — largest single outsourcing gap |

| IT Consulting & Staffing | Very High | NOT taxable | Technology consulting, IT staff augmentation, offshore development teams, application development services |

| Human Resources Outsourcing | High | NOT taxable | HR administration, recruiting, benefits management, PEO services, employee training |

| General Business Process Outsourcing (BPO) | Very High | NOT taxable | Call centers, back-office operations, supply chain management, customer service operations — the largest global outsourcing category |

The most significant pattern in this analysis is that the categories with the highest foreign outsourcing relevance — professional services, IT consulting, HR outsourcing, and general BPO — are precisely the ones not currently taxable under Texas law. This is not a coincidence. These exemptions are largely the product of decades of lobbying by professional associations and industry groups. The TPTRP’s fundamental commitment to no exemptions means all of these high-value, high-volume outsourcing categories will be brought into the tax base for the first time. That is where the foreign entity framework becomes most important, because these are also the service categories most heavily supplied by foreign providers.

Multi-State Apportionment: Services Used Both In and Outside Texas

A practical question for any multi-state or cross-border business: what happens when a service is consumed by a Texas business that operates in multiple states? The answer is already established in Texas law — only the portion of the service used in Texas is subject to Texas sales tax. For data processing services, if the service cannot be assigned to an identifiable segment of the client’s business, it is sourced to the client’s principal place of business.

The 2025 amendments to Texas Administrative Code Section 3.330 updated and clarified multi-state allocation rules for data processing services and added new definitions for bundled transactions. The TPTRP legislation will extend these apportionment principles to all newly taxable service categories, ensuring that foreign entities providing services consumed in multiple states are taxed only on the Texas-use portion — satisfying the fair apportionment prong of the Complete Auto Transit test and preventing unconstitutional double taxation.

Legislative Action Required: Services Base Expansion

Before the foreign entity collection mechanism has anything meaningful to collect, the TPTRP must first expand the taxable services base in Texas Tax Code § 151.0101 to include professional services, IT consulting and staffing, HR outsourcing, and general BPO. The foreign entity portal and registration system apply the tax; the services base expansion defines what is taxable. Both are essential, and both must be enacted together.

Global Precedents: How Other Jurisdictions Do This

The EU One Stop Shop, OECD international standards, the federal HIRE Act, and more than 110 countries that already collect tax from foreign service providers — the proof of concept is global

Texas does not need to invent a system from scratch. The challenge of collecting consumption taxes from foreign service providers has been solved — elegantly and at scale — by jurisdictions around the world. The leading model is the European Union’s One Stop Shop (OSS), which since 2021 has handled VAT collection from non-EU businesses across 27 member states through a single registration and filing portal. Understanding how these systems work is essential to designing the Texas Foreign Entity Sales Tax Portal correctly.

The EU One Stop Shop Non-Union Scheme: The Gold Standard

The EU’s Non-Union OSS Scheme is specifically designed for businesses established outside the EU that supply services to EU consumers. A foreign business registers once with a single EU member state — its “Member State of Identification” — collects VAT at the rate applicable in each customer’s country, files one consolidated quarterly return, and makes one payment. The Member State of Identification then distributes the revenue to the appropriate countries. The entire system is online, multi-lingual, and does not require the foreign business to establish a legal entity in any EU country.

This is exactly the model the TPTRP should adopt for Texas: a single Comptroller portal, destination-based collection at the Texas rate applicable to the customer’s location, quarterly consolidated filing, and single remittance. The EU OSS went live on July 1, 2021, and replaced the prior Mini One Stop Shop (MOSS) system that had operated for digital services since 2015. The EU’s experience demonstrates that this model works at scale, can be built and operated by a government tax authority, and is accepted by the international business community as a legitimate compliance obligation.

Global Models for Foreign Service Provider Tax Collection

Selected jurisdictions requiring foreign entities to register, collect, and remit consumption tax on services — with design features directly applicable to the TPTRP portal

| Jurisdiction | Rate | Mechanism | Filing | TX-Applicable Design Features |

|---|---|---|---|---|

| EU (27 states) | 15–27% (by country) | OSS Non-Union Scheme | Quarterly | Single registration in one country; automatic distribution to all customer states; covers all services; no local entity required |

| United Kingdom | 20% | Non-Union VAT Registration | Quarterly | Separate from EU post-Brexit; streamlined for non-UK businesses; online-only portal |

| Australia | 10% GST | Simplified GST Registration | Quarterly | Low compliance burden; streamlined online portal; no local entity required; covers digital services and some goods |

| Canada (fed.) | 5% GST | Simplified GST/HST | Annual | Federal simplified regime for non-residents; provincial rules vary |

| Singapore | 9% GST | Overseas Vendor Registration (OVR) | Quarterly | Covers B2B and B2C; platform operators required to collect on behalf of foreign sellers; robust enforcement |

| South Korea | 10% VAT | Foreign Simplified Registration | Quarterly | Electronic services focus; major platform operators register on behalf of foreign sellers; no threshold |

| New Zealand | 15% GST | Non-Resident Registration | Two-monthly | Covers remote services and low-value imported goods; streamlined online portal |

| Texas (TPTRP) | TPTRP Rate | TX Foreign Entity Sales Tax Portal | Quarterly | Single registration, destination-based by customer ZIP, online remittance, multilingual, no U.S. entity required, VDA program |

The OECD’s International Standards

The Organisation for Economic Co-operation and Development has published internationally recognized standards for how countries should impose consumption taxes on digital services provided by non-resident suppliers. The OECD’s VAT Digital Toolkit establishes the destination-based approach — tax is owed where the consumer is located — as the global standard. This aligns precisely with Texas’s existing destination-based sourcing rules for remote sellers.

The OECD specifically recommends: simplified registration regimes requiring no local entity registration; threshold-based collection obligations (parallel to Texas’s $500,000 standard); online portals with multilingual support and rate calculation tools; marketplace facilitator rules shifting collection responsibility to digital platforms; and reverse-charge mechanisms for B2B transactions. All of these design elements are directly incorporated into the TPTRP foreign entity portal specification in Section 6 below. Texas is not departing from international norms — it is aligning with them.

The Federal HIRE Act: Related But Not Competing

In September 2025, the U.S. Senate introduced the Halting International Relocation of Employment (HIRE) Act, proposing a 25% federal excise tax on outsourcing payments made by U.S. companies to foreign persons for labor or services benefiting U.S. consumers. The bill would also deny income tax deductions for such payments and would direct revenues to a domestic worker retraining fund.

For TPTRP purposes, the HIRE Act is important to understand precisely because it is not in conflict with the TPTRP’s foreign entity sales tax. The HIRE Act is a federal excise tax imposed on the U.S. buyer for the act of making outsourcing payments to foreign entities — it is a transaction tax on the buyer. The TPTRP sales tax is a state consumption tax collected by the seller on the value of the service transaction. They operate at different levels of government (federal vs. state), on different parties (buyer vs. seller), with different purposes and different legal authority. Both can exist simultaneously without conflict, and the HIRE Act’s pending legislative status does not affect the TPTRP’s design or constitutional soundness.

The Current Texas Secretary of State Registration Framework

Texas already requires certain foreign entities “transacting business” in Texas to register with the Secretary of State under Chapter 9 of the Texas Business Organizations Code. However, this standard is built around physical presence activities and does not cleanly map to economic nexus for sales tax purposes. Many foreign entities providing remote outsourcing services to Texas clients would not be required to register with the SOS — even though they may have economic nexus for sales tax purposes. The TPTRP Foreign Entity Sales Tax Portal is a separate registration system administered by the Comptroller, distinct from the SOS corporate registration requirement. Registering on the tax portal does not, by itself, constitute “transacting business” under the Business Organizations Code or create corporate law obligations.

The Texas Foreign Entity Sales Tax Portal

Complete operational design: registration, rate calculation, filing, remittance, marketplace facilitator rules, and a six-layer enforcement strategy

Establishing legal authority is necessary but not sufficient. The practical question is how to make it work for an entity in Manila, Mumbai, or Manchester: how do they know what they owe, how to register, what rate to charge, and how to pay? The answer is a purpose-built, online-first compliance portal modeled on the EU’s proven One Stop Shop system and designed specifically for entities that have no physical presence in Texas or the United States. The TPTRP legislation will authorize and fund this portal as a Comptroller-operated system.

Who Must Register and When

The registration trigger is Texas’s existing economic nexus threshold: any entity — domestic, out-of-state, or foreign — whose total Texas revenue from taxable goods or services exceeds $100,000 in the preceding 12 calendar months must register under the TPTRP framework. Registration must be completed before making the first taxable sale after the threshold is crossed. There is no grace period. However, the Voluntary Disclosure Program (described below) provides historical relief for entities that come forward proactively before being contacted by the Comptroller.

Registration: What Foreign Entities Need

Registration through the Texas Foreign Entity Sales Tax Portal will not require: a U.S. Social Security Number or Individual Taxpayer Identification Number; registration with the Texas Secretary of State as a foreign entity (a separate and distinct corporate law obligation); or a U.S. bank account. Foreign entities will use their home-country tax identification number, or where none exists, will receive a Texas Comptroller-assigned Foreign Entity Sales Tax ID. Upon successful registration, the entity receives a Texas Remote Sales Tax Permit (Foreign Entity Designation) — a new permit category distinct from the standard Texas Sales and Use Tax Permit issued to physical-presence businesses.

Required registration information: entity legal name, country of domicile and principal business address, primary contact name and information, description of services provided to Texas customers, estimated annual Texas revenue, home-country tax identification number, and payment account information for remittances. The portal will be available in English and Spanish at minimum, with Mandarin, Hindi, Portuguese, and Filipino added for the primary outsourcing source countries.

Rate Determination: Destination-Based by Customer ZIP Code

Texas uses destination-based sourcing for remote sellers: tax is calculated based on the customer’s location, not the seller’s. For a foreign entity serving a Texas customer in Cedar Hill, the applicable rate is the combined state and local rate for Cedar Hill, which varies by the customer’s precise location within the taxing jurisdiction. The TPTRP portal will include a built-in rate lookup tool by customer ZIP code and service category, eliminating the need for foreign entities to independently research applicable local tax rates. This is identical to the rate lookup tools that the EU member states provide within the OSS portal and that Avalara and similar services offer commercially.

Filing and Remittance: Quarterly, Consolidated, Online

Filing will be quarterly, consistent with the international standard. Foreign entities will submit a single consolidated return covering all Texas taxable sales for the period, report total tax collected by local rate jurisdiction, and make a single payment covering all obligations. The portal will accept: ACH electronic funds transfer (for entities with U.S. bank accounts), international wire transfer, and major international electronic payment platforms designated by the Comptroller. No paper filing will be accepted. Entities falling below $500,000 in Texas revenue for 12 consecutive months may apply to deregister.

Marketplace Facilitator Rules Extended to Services

Texas already applies marketplace facilitator rules to tangible goods: platforms that facilitate third-party vendor sales are responsible for collecting and remitting tax on those vendors’ behalf. The TPTRP will explicitly extend these rules to services. Digital platforms that connect Texas businesses with foreign or out-of-state service providers — freelance marketplaces, BPO matching platforms, cloud service brokers, staffing platforms — will be designated as marketplace facilitators and required to collect and remit on behalf of their foreign sellers. This single mechanism will capture the long tail of smaller foreign service providers who individually fall below the $500,000 threshold, because the marketplace facilitator consolidates their Texas revenues into a single taxable relationship with the Comptroller.

Rate Integration with the TPTRP Rate Structure

The foreign entity sales tax will be integrated into the TPTRP’s tiered rate structure. B2B outsourcing transactions — services purchased by Texas businesses from foreign entities for use in their business operations — will be subject to the standard TPTRP commercial transaction rate, consistent with the TPTRP’s elimination of B2B exemptions. A foreign entity providing services that will be incorporated into the Texas business’s own taxable service sales may accept a resale certificate, consistent with current Texas law, avoiding unconstitutional tax pyramiding within the supply chain.

The Six-Layer Enforcement Strategy

Enforcement against non-compliant foreign entities is the primary practical challenge. Entities physically outside U.S. borders cannot be directly compelled through Texas courts in the same way as domestic entities. The TPTRP addresses this through a layered enforcement strategy that does not depend solely on direct action against the foreign entity:

- Texas Buyer-Side Reporting: Texas businesses claiming a deduction or business expense for payments to foreign or out-of-state service providers above $10,000 per year must certify on their TPTRP return that either: (a) the vendor holds a valid Texas Remote Sales Tax Permit and collected Texas tax; or (b) the buyer has self-assessed and remitted use tax on the transaction. Failure to certify creates a rebuttable presumption that use tax is owed, and the Comptroller may assess accordingly. This converts the Texas buyer into an enforcement partner with a direct financial incentive to ensure their foreign vendors are in compliance.

- Use Tax Backstop: Texas law already provides that if a seller fails to collect, the buyer owes use tax directly to the Comptroller. The TPTRP strengthens this mechanism by making buyer certification a required element of the business return, transforming a passive legal obligation into an active reporting requirement.

- IRS Data Sharing: The Comptroller will enter a data-sharing agreement with the Internal Revenue Service to access Forms 1099 and 1042-S identifying payments by Texas-domiciled payers to foreign service providers. These federal information returns, filed by U.S. businesses making payments to foreign vendors, create a readily available database for identifying non-compliant foreign entities who are receiving significant Texas-source income without a Texas permit on file.

- Marketplace Facilitator Coverage: By extending marketplace facilitator rules to services platforms, the TPTRP captures the majority of foreign service transactions through U.S.-based platform operators who are fully within Texas enforcement jurisdiction. The platform operator faces direct Texas liability for collection failures, creating a commercial incentive for platforms to require their foreign vendors to comply or be removed from the platform.

- Banking Reporting: Authorize the Comptroller to receive reports from Texas-chartered banks and branches of foreign banks operating in Texas identifying international wire transfers to foreign service providers above a reporting threshold where the transferor does not have a Texas Remote Sales Tax Permit on file. This closes the gap for large, direct transactions outside any platform.

- Voluntary Disclosure Program: A structured Voluntary Disclosure Agreement (VDA) program for foreign entities not currently compliant, offering: a look-back period limited to not more than four years; penalty waivers for periods covered by the voluntary disclosure; and streamlined registration and filing. The VDA program will remain open on a continuing basis. This is statistically the most cost-effective enforcement tool — it brings the largest number of non-compliant entities into compliance at the lowest administrative cost, and the international precedent shows that well-designed VDA programs capture the majority of voluntary compliance.

The Three Walls: Locking Out Non-Compliant Foreign Sellers

The TPTRP foreign entity framework is built on three interlocking enforcement walls, not a single registration requirement. Understanding all three is essential to understanding why this framework is meaningfully different from the weak use-tax system it replaces.

Wall One — The Seller Registration Gate (SOS + Comptroller Permit)

Under the implementing bill (Section 6), the Secretary of State registration prerequisite is written into the Texas Business Organizations Code as a condition of market access. A foreign or out-of-state entity cannot lawfully do business in Texas without that registration, which is in turn tied to Comptroller permit status. An unregistered foreign entity therefore cannot enforce contracts in Texas courts, cannot sue Texas customers for non-payment, and cannot legally sustain Texas business relationships. This makes non-registration legally expensive for the seller — not merely inconvenient.

Wall Two — The Texas Buyer Prohibition (Civil and Criminal Liability)

Section 10 of the implementing bill creates a hard statutory prohibition: a Texas business is legally barred from transacting with an unregistered out-of-state or foreign entity when that entity should be collecting and remitting the Unified Transaction Tax. The Texas buyer has an affirmative verification duty — before transacting, it must confirm the vendor holds a valid Texas Comptroller permit. If it transacts anyway, it owes the uncollected tax plus interest, and faces escalating civil penalties: 25% of tax liability for a first violation, 50% for a second, and 100% for a third or subsequent violation. Its own Comptroller permit can be suspended for up to 12 months for first violations.

Section 12 adds criminal exposure for any officer or director who knowingly directs a Texas business to transact with an unregistered foreign entity: a Class B misdemeanor if total tax liability does not exceed $5,000, and a Class A misdemeanor if it does. This reaches the decision-makers personally — not just the corporate entity — which gives the prohibition real deterrent force.

Wall Three — The Public Registry

Section 7 of the implementing bill requires the Texas Foreign Entity Transaction Tax Portal to maintain a searchable Public Registry of all registered remote and foreign sellers. Any Texas buyer can look up any vendor before transacting and confirm permit status. This makes compliance visible, verification easy, and willful non-verification legally indefensible. The registry also gives Comptroller auditors a ready tool for identifying unregistered sellers operating in the Texas market who should be registered.

Statute of Limitations Tolling

Section 11(d) of the implementing bill provides that the statute of limitations for assessment is tolled for any period during which a foreign entity was required to register but did not. A foreign business cannot simply hide for years, wait for the limitations period to expire, and then claim it is too late for the Comptroller to collect. The clock does not run while the entity is out of compliance.

Marketplace Facilitator Coverage

Foreign entities that deliver services through a platform — outsourcing marketplaces, staffing platforms, software service brokers — are caught by marketplace facilitator rules extended to services (Section 8). The platform becomes the collecting entity, responsible for remitting on behalf of its foreign vendors. A foreign seller cannot route around the collection obligation by operating through a digital intermediary.

What This Means for Texas Businesses

The compliance obligation does not sit solely on the foreign vendor. Every Texas business that purchases taxable services from a foreign or out-of-state vendor has a verification duty and faces real legal consequences for knowingly circumventing it. The framework is designed so that the Texas market itself becomes inhospitable to unregistered foreign sellers — because every Texas customer they have is legally motivated to require their compliance.

Legal Risk Analysis and Mitigations

An honest assessment of every meaningful constitutional and legal challenge the TPTRP’s foreign entity framework may face — with specific design mitigations for each

A proposal of this significance will face legal challenges — from foreign companies, from advocacy groups, and potentially from foreign governments through diplomatic channels. The TPTRP must be designed from the outset to withstand those challenges. The following analysis addresses every meaningful legal risk, assesses its severity based on settled precedent, and identifies the specific legislative design features that mitigate each risk. Legislators, legal counsel, and constituents deserve full transparency on what the risks are and how they are being addressed.

Constitutional and Legal Risk Assessment — TPTRP Foreign Entity Framework

All significant legal challenges, risk levels based on settled precedent, and specific legislative mitigations

| Legal Risk | Risk Level | Controlling Authority | Specific Mitigation in Legislation |

|---|---|---|---|

| Import-Export Clause challenge | LOW | Clause applies only to goods; services excluded per settled case law since Woodruff v. Parham (1869) through modern Cornell LII and LOC analysis | Legislation expressly applies only to services and non-goods transactions; statutory language carves out goods subject to federal customs duties |

| Commerce Clause (interstate) | LOW | Wayfair (2018) settles economic nexus; Complete Auto 4-prong test satisfied by non-discriminatory flat rate applied uniformly | Identical rates and rules for all remote sellers regardless of state of domicile; $100,000 TPTRP threshold consistent with the Wayfair safe-harbor pattern; more protective than current Texas $500K baseline |

| Foreign Commerce Clause — Discrimination | MODERATE | Japan Line (1979) and Barclays (1994) require non-discriminatory treatment of foreign entities | Identical rate and rules for all foreign sellers; zero country-specific treatment; zero discriminatory foreign surcharges; facially neutral legislation |

| Foreign Commerce Clause — Multiple Taxation | MODERATE | Risk if other jurisdictions tax the same transaction on similar basis; Japan Line prong 5 | Clear apportionment rules in legislation; Comptroller authorized to provide inter-jurisdictional credits to prevent unconstitutional double taxation |

| Federal Tax Treaty Preemption | NONE / LOW | Federal income tax treaties expressly govern federal income tax only; states not parties; confirmed by BNN CPA, PKF O’Connor Davies, and Anchin Advisory analysis | Statutory findings section documents that federal tax treaties do not apply to state sales taxes; Comptroller guidance will clarify for foreign entities |

| Due Process / Minimum Contacts | LOW | $500,000 in Texas revenue far exceeds any reasonable minimum contacts threshold post-Wayfair | $500K threshold ensures robust commercial connection before obligation attaches; threshold represents deliberately sought Texas market access |

| HIRE Act Conflict | NONE | Federal excise on the buyer; state sales tax on the seller; entirely different parties, governments, and legal bases | No legislative action needed to avoid conflict; HIRE Act status to be monitored as a data point on federal legislative direction |

| “Speaks With One Voice” Doctrine | MODERATE | Barclays (1994): requires actual congressional preemption, not merely executive or diplomatic objection; non-discriminatory tax generally survives | Universal non-discriminatory application; treaty monitoring provision in legislation; Comptroller authorized to yield to any future congressional directive governing state taxation of foreign commerce |

| Practical Enforcement Against Non-Compliant Foreign Entities | HIGH (practical) | No federal precedent for compelling foreign entities outside U.S. jurisdiction through Texas courts directly; primary practical risk is collection deficiency, not legal invalidity of the tax | Six-layer enforcement strategy: buyer-side reporting, use tax backstop, IRS 1042-S data sharing, marketplace facilitator rules, banking reporting, and Voluntary Disclosure Program |

The Bottom Line on Constitutional Soundness

The TPTRP foreign entity framework is constitutionally sound when designed as specified in this article and the accompanying draft legislation. The legal risks are real and must be respected in the legislative drafting, but none of them represents a fundamental barrier to the framework. The two most important design rules — which must be treated as absolute requirements, not suggestions — are: (1) identical rates and rules for all sellers regardless of national origin; and (2) fair apportionment for services consumed in multiple states or countries. Get those two things right, and the constitutional framework holds.

What the TPTRP Constitutional Amendment Must Address

The constitutional amendment eliminating property taxes and authorizing the TPTRP sales tax must include express language on four points: (1) universal application of the sales tax to all commercial transactions consumed in Texas regardless of seller location; (2) explicit abrogation of the physical presence requirement at the state constitutional level; (3) authorization for the Legislature to define “engaged in business in Texas” based on economic activity; and (4) a non-discrimination mandate preventing future Legislatures from creating discriminatory foreign surcharges. The completed constitutional amendment (H.J.R. No. _____, 90th Legislature) covers all four requirements plus two additional protections: the Definition Filter establishing which transactions are outside Texas jurisdiction, and a constitutional floor on the non-discrimination and anti-exemption requirements that prevents a future Legislature from restoring special-interest carve-outs for foreign or out-of-state sellers. The implementing bill (H.B. No. _____) then operationalizes all of these constitutional mandates through registration, portal, enforcement, and penalty mechanisms.

TPTRP Foreign Entity and Remote Seller Compliance Legislation

Rep. Will Campbell · House District 109 · Texas 90th Legislative Session — Two draft bills. Bill 1 is the enabling statute. Bill 2 provides the constitutional amendment language for the foreign entity provision to be incorporated into the main TPTRP constitutional amendment when drafted.

By: ___________________ H.B. No. _____

A BILL TO BE ENTITLED

AN ACT

relating to the collection, registration, administration, and remittance of the unified transaction tax by remote sellers and foreign entities transacting business in this state; requiring out-of-state and foreign entities to register with the Secretary of State and obtain a Comptroller tax permit before transacting business with Texas customers; prohibiting Texas businesses from transacting with unregistered out-of-state or foreign entities; establishing the Texas Foreign Entity Transaction Tax Portal; replacing the enumerated taxable services list with a broad-base all-services standard; repealing specified Tax Code Chapter 151 exemptions inconsistent with the broad-base design; excluding Internet access service from the unified transaction tax base as required by federal law; extending marketplace facilitator obligations to services; providing civil and criminal penalties; providing a voluntary disclosure program; and making conforming amendments to the Texas Tax Code and the Texas Business Organizations Code; imposing a tax.

BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF TEXAS:

SECTION 1. SHORT TITLE.

This Act may be cited as the "Remote Seller and Foreign Entity Unified Transaction Tax Act."

SECTION 2. LEGISLATIVE FINDINGS AND PURPOSE.

(a) The Legislature finds that:

(1) Section 1-p, Article VIII, Texas Constitution, as added by H.J.R. No. _____, 90th Legislature, Regular Session, 2027, establishes the Unified Transaction Tax as a broad-base, destination-based tax on all taxable transactions in this state, applicable to all sellers regardless of physical location or domicile, at every point in the supply chain, at a uniform rate that does not vary by seller domicile;

(2) Section 1-q, Article VIII, Texas Constitution, as added by H.J.R. No. _____, establishes the economic nexus standard and the registration prerequisites — including Secretary of State authorization and a Comptroller tax permit — that apply to all remote sellers, including out-of-state and foreign entities, as a constitutional minimum;

(3) a significant and growing volume of commercial transactions conducted with Texas businesses and consumers is provided by foreign entities and out-of-state entities that do not currently collect or remit Texas sales and use tax on those transactions, creating a material revenue gap and an inequitable competitive disadvantage for Texas-domiciled businesses;

(4) the Supreme Court of the United States in *South Dakota v. Wayfair, Inc.*, 585 U.S. 162 (2018), confirmed that a state may impose a sales and use tax collection obligation on a remote seller that lacks physical presence in the state and that economic nexus based on the volume of sales into the state is the appropriate constitutional standard;

(5) federal income tax treaties between the United States and foreign countries govern only federal income taxation and do not preempt, limit, or affect state sales and use tax obligations; states are not parties to such treaties, and foreign entities subject to such treaties remain fully subject to the Unified Transaction Tax;

(6) the Import-Export Clause of the United States Constitution (Article I, Section 10, Clause 2) applies only to tangible goods at the point of importation and does not apply to services, digitally delivered products, or subsequent sales of imported goods within this state; the Unified Transaction Tax on services and in-state transactions is not a tax on importation and is not subject to the Import-Export Clause;

(7) the Unified Transaction Tax is a general broad-base transaction tax imposed at a uniform rate on all taxable transactions regardless of whether the transaction is conducted online, in person, by telephone, by mail, or through any other medium or channel of commerce; the Unified Transaction Tax does not impose a tax on electronic commerce that is not also imposed on equivalent transactions conducted through other means; it therefore does not constitute a discriminatory tax on electronic commerce prohibited by the Internet Tax Freedom Act, 47 U.S.C. § 151 note;

(8) Internet access service — the service of connecting a user to the Internet — is excluded from the Unified Transaction Tax base as required by the permanent prohibition in the Internet Tax Freedom Act; content, applications, and digital services delivered over the Internet are not Internet access service and are taxable transactions;

(9) the use-tax self-assessment mechanism under prior law was rarely enforced and created a systemic compliance gap; the buyer prohibition established by this Act eliminates that gap and places all sellers on equal footing as a condition of market access;

(10) the Secretary of State registration prerequisite placed on out-of-state and foreign entities by this Act is a non-discriminatory, content-neutral market-access condition identical in character to requirements already imposed on Texas-domiciled businesses; it is consistent with the Commerce Clause, the Foreign Commerce Clause, *Complete Auto Transit, Inc. v. Brady*, 430 U.S. 274 (1977), and *National Pork Producers Council v. Ross*, 598 U.S. 356 (2023), which confirmed that non-discriminatory state regulations do not violate the dormant Commerce Clause merely because they affect out-of-state conduct;

(11) every remote seller meeting the economic nexus threshold of Section 1-q(a), Article VIII, Texas Constitution, benefits from the services, infrastructure, legal system, and commercial marketplace of this state — including access to Texas courts, the protection of Texas commercial law, Texas transportation and communications infrastructure enabling delivery, and the Texas consumer market — in a manner sufficient to justify the obligations imposed by this Act; this finding satisfies the fair relationship prong of *Complete Auto Transit, Inc. v. Brady*;

(12) the obligations imposed by this Act on foreign entities apply equally to all foreign entities regardless of country of domicile and do not impair the federal government's ability to speak with one voice in foreign affairs; a uniform, non-discriminatory destination-based consumption tax of the type established by this Act does not conflict with any federal foreign policy interest and is consistent with the foreign commerce clause requirements of *Japan Line, Ltd. v. County of Los Angeles*, 441 U.S. 434 (1979), and *Barclays Bank PLC v. Franchise Tax Board*, 512 U.S. 298 (1994); and

(13) the establishment of a simplified, single-point foreign entity registration and remittance portal will facilitate compliance and is consistent with internationally recognized best practices for cross-border consumption tax administration, as reflected in the European Union's One Stop Shop system and OECD VAT Digital Toolkit standards.

(b) The purpose of this Act is to implement Sections 1-p and 1-q, Article VIII, Texas Constitution, by:

(1) establishing the economic nexus threshold and the registration and remittance obligations of all remote sellers;

(2) replacing the enumerated taxable services list in Tax Code §151.0101 with a broad-base all-services standard consistent with Definition 1 of the Unified Transaction Tax;

(3) repealing specified Tax Code Chapter 151 exemptions — including the intercorporate services exemption, the sales-for-resale certificate system, the manufacturing-input exemption, and certain industry-specific exemptions — that are inconsistent with the broad-base design of the Unified Transaction Tax and prohibited by Section 1-p(h), Article VIII, Texas Constitution;

(4) expressly excluding Internet access service from the Unified Transaction Tax base as required by the Internet Tax Freedom Act;

(5) requiring all out-of-state and foreign entities to register with the Secretary of State and obtain a Comptroller tax permit before transacting business with Texas customers;

(6) prohibiting Texas businesses from transacting with unregistered out-of-state or foreign entities and providing penalties for violations;

(7) establishing the Texas Foreign Entity Transaction Tax Portal as the single-point compliance system for remote sellers; and

(8) providing enforcement mechanisms, penalties, and a voluntary disclosure program sufficient to ensure universal compliance.

SECTION 3. DEFINITIONS.

In this Act:

(1) "Unified Transaction Tax" means the broad-base, destination-based transaction tax established by Section 1-p, Article VIII, Texas Constitution, imposed on all taxable transactions in this state.

(2) "Taxable transaction" has the meaning established by Section 1-p(b), Article VIII, Texas Constitution — a transaction in which a clear product is being purchased or a service is being rendered, at every point in the supply chain, where the buyer is located in this state or the economic benefit is received in this state. The term does not include transactions excluded by the Definition Filter under Section 1-p(e), Article VIII, Texas Constitution.

(3) "Agent transaction" has the meaning established by Section 1-p(c), Article VIII, Texas Constitution — a transaction in which a person acting as agent on behalf of a principal purchases a product or service on the principal's behalf and separately renders the agent's own labor or product to the principal, subject to the anti-pyramiding rule.

(4) "Remote seller" means any person or entity that makes taxable transactions with Texas customers without maintaining a primary place of business in Texas, including:

(A) businesses incorporated, domiciled, or registered in another state of the United States; and

(B) foreign national entities incorporated, domiciled, or organized under the laws of a country other than the United States.

(5) "Foreign entity" means any person, corporation, partnership, limited liability company, trust, or other legal entity that is domiciled, incorporated, or organized under the laws of a country other than the United States.

(6) "Texas customer" means any natural person, business entity, organization, or governmental body that:

(A) maintains a physical address, place of business, or place of residence in this state; or

(B) receives the economic benefit of a transaction at a location in this state; or

(C) is billed to a Texas address for the goods or services received;

provided that, for a transaction with a foreign entity or out-of-state entity, the foreign entity or out-of-state entity knew or reasonably should have known, at the time of contracting or delivery, that the goods or services would be used, consumed, or primarily benefiting operations or persons located in this state.

(7) "SOS Authorization" means the registration, certificate of authority, or other authorization issued by the Secretary of State to an out-of-state or foreign entity authorizing that entity to transact business in this state.

(8) "Texas Tax Registration Certificate" means the certificate issued by the Comptroller to a remote seller that has satisfied the registration and permit requirements of this Act, authorizing that entity to collect and remit the Unified Transaction Tax.

(9) "Portal" means the Texas Foreign Entity Transaction Tax Portal established under Section 7 of this Act.

(10) "Comptroller" means the Comptroller of Public Accounts of the State of Texas.

(11) "Secretary of State" means the Secretary of State of the State of Texas.

(12) "Outsourced services" means services acquired by a Texas business from a seller located outside this state — whether in another state of the United States or in a foreign country — where those services are performed primarily for the benefit of the Texas business's Texas operations, customers, or workforce, and where the seller knew or reasonably should have known that the services would benefit Texas operations.

(13) "Internet access service" means the service of connecting a subscriber or user to the Internet through a broadband, wireless, dial-up, satellite, or any other access technology, including any directly bundled telecommunications service used to provide the access connection. The term does not include content, applications, data services, or digital products delivered over the Internet. Internet access service is excluded from the Unified Transaction Tax base under Section 1-p(e)(4), Article VIII, Texas Constitution, and is not a taxable transaction under this Act.

(14) "Marketplace facilitator" means a person that operates a digital platform, software application, or electronic marketplace that lists, advertises, or makes available taxable services or goods offered by third-party providers to purchasers in this state; facilitates the transaction between the provider and the purchaser; and collects or directs the collection of payment from the purchaser.

SECTION 4. AMENDMENT TO TEXAS TAX CODE §151.008 — ECONOMIC NEXUS STANDARD.

(a) Section 151.008, Texas Tax Code, is amended by adding Subsections (c) and (d) to read as follows:

(c) For purposes of this chapter, a person is "engaged in business in this state" if, during the preceding 12 calendar months, the person:

(1) made taxable transactions with Texas customers totaling $100,000 or more in gross receipts; or

(2) made 200 or more separate taxable transactions with Texas customers;

regardless of whether the person:

(A) has a physical presence of any kind in this state;

(B) is incorporated or organized under the laws of this state or any other state; or

(C) is domiciled, incorporated, organized, or registered under the laws of any country other than the United States.

(d) Subsection (c) applies without limitation to any natural person, corporation, partnership, limited liability company, association, joint venture, trust, or other entity organized or domiciled under the laws of any jurisdiction, domestic or foreign.

(b) The economic nexus thresholds established by Subsection (c), Section 151.008, Texas Tax Code, as added by this section, are the maximum thresholds permitted under Section 1-q(a), Article VIII, Texas Constitution. The Comptroller may, by rule, establish lower thresholds.

SECTION 5. REPLACEMENT OF TEXAS TAX CODE §151.0101 — BROAD-BASE TAXABLE SERVICES.

(a) Section 151.0101, Texas Tax Code, is amended to read as follows:

Sec. 151.0101. TAXABLE SERVICES.

(a) "Taxable services" means all services rendered for consideration to a Texas customer, as defined by Section 1-p(b), Article VIII, Texas Constitution, regardless of:

(1) the industry, business sector, or NAICS classification of the provider or the recipient;

(2) whether the service is provided in person, remotely, electronically, digitally, or through any other means or medium;

(3) whether the service is provided to a consumer or to a business;

(4) whether the service provider is located in this state, in another state, or in a foreign country; or

(5) the form or name by which the service is described in any contract, invoice, or marketing material.

(b) The term "taxable services" includes without limitation:

(1) professional services, including legal, accounting, bookkeeping, management consulting, business strategy, financial advisory, engineering, architectural, environmental consulting, actuarial, and similar services requiring specialized professional knowledge;

(2) information technology and digital services, including software development, application development and maintenance, technology consulting, systems integration, information technology staff augmentation, cloud computing, data processing, cybersecurity, data analytics, and related technology implementation or advisory services; content, applications, and digital products delivered electronically are taxable services; Internet access service is not a taxable service and is excluded under Section 1-p(e)(4), Article VIII, Texas Constitution;

(3) human resources services, including recruitment, staffing, human resources administration, employee benefits management, payroll preparation, training and development, and professional employer organization services;

(4) business process services, including call center and contact center operations, back-office operations, supply chain management, procurement, customer service operations, and general administrative services;

(5) real property services, including construction services, real property repair and remodeling, facilities management, janitorial and maintenance services, and construction management services; the exclusion of real property transfers from the Definition Filter does not exempt real property services from this chapter;

(6) digital content, streaming, and subscription services, including streaming video, streaming audio, online gaming, software subscription services, and any other digital product or service delivered electronically and consumed in this state; and

(7) all other commercial services provided for consideration where the service is consumed, used, or directed to a person or entity located in or doing business in this state, consistent with Definition 1 of the Unified Transaction Tax established by Section 1-p(b), Article VIII, Texas Constitution.

(c) The term "taxable services" does not include:

(1) Internet access service, as defined by Section 3(13) of the Remote Seller and Foreign Entity Unified Transaction Tax Act, which is excluded from the Unified Transaction Tax base under Section 1-p(e)(4), Article VIII, Texas Constitution, and by the Internet Tax Freedom Act, 47 U.S.C. § 151 note; and

(2) transactions excluded by the Definition Filter under Section 1-p(e), Article VIII, Texas Constitution — federal government transactions, financial flows as defined in Category F, intra-company transfers as defined in Category I-1, and cryptocurrency used solely as a payment instrument.

(d) The Texas Living Exemption Set established under Article [Y] of the Texas Property Tax Replacement Plan constitutional amendment governs which transactions that otherwise qualify as taxable transactions are exempt from the Unified Transaction Tax for qualified cost-of-living purposes. No exemption from the Unified Transaction Tax may be created by the Legislature other than as provided by the Texas Living Exemption Set or by constitutional amendment, consistent with Section 1-p(h), Article VIII, Texas Constitution.

(e) The Comptroller shall promulgate rules clarifying the application of this section to specific services and establishing apportionment methodologies for services consumed both within and outside this state.

(b) The enumerated list of taxable services previously contained in Section 151.0101, Texas Tax Code, before amendment by this Act is superseded in its entirety by the broad-base all-services standard established by this section. No service that was taxable under prior law is rendered untaxable by this amendment. All services taxable under prior law remain taxable. Additional services are taxable as provided by this section.

SECTION 5A. CONFORMING REPEALS — TAX CODE CHAPTER 151 EXEMPTIONS INCONSISTENT WITH THE UNIFIED TRANSACTION TAX.

(a) The following sections of Chapter 151, Texas Tax Code, are repealed effective upon voter approval of H.J.R. No. _____, 90th Legislature, Regular Session, 2027, and the taking effect of this Act:

(1) Section 151.346 (Intercorporate Services) is repealed. The exemption for service transactions among affiliated entities that report income to the IRS on a consolidated return is inconsistent with Section 1-p(h), Article VIII, Texas Constitution, which prohibits intercorporate services exemptions, and with Definition 1 of the Unified Transaction Tax, which applies at every point in the supply chain including business-to-business transactions. Services rendered by one legal entity to another legal entity are taxable transactions regardless of their corporate affiliation or consolidated tax filing status.

(2) Section 151.302 (Sale for Resale — Certificate System) is repealed to the extent it creates a resale certificate exemption mechanism. The resale certificate system is replaced by the Agent Transaction Anti-Pyramiding Rule established by Section 1-p(c), Article VIII, Texas Constitution. No resale certificate shall be issued or accepted after the effective date of this Act. Transactions that would have been exempt under the resale certificate system are governed instead by the anti-pyramiding rule: goods or services acquired for resale are taxed once at acquisition; the resale itself is a separate taxable transaction taxed once at the point of the resale. The net effect is that each dollar of economic value is taxed once — at the point of each actual transaction — with no exemption at any stage of the supply chain.

(3) Section 151.318 (Manufacturing Inputs) is repealed. Manufacturing-input exemptions are prohibited by Section 1-p(h), Article VIII, Texas Constitution. All inputs purchased by a manufacturer — raw materials, components, supplies, equipment, and services — are taxable transactions at the point of purchase. The anti-pyramiding rule of Section 1-p(c) ensures no dollar is taxed more than once across the supply chain.

(4) Section 151.351 (Information Services — Partial Exemption / 80-20 Data Processing Split) is repealed to the extent it provides that any percentage of data processing or information services is exempt from tax. All data processing services, information services, and SaaS, PaaS, IaaS, and related cloud computing services are taxable in full as taxable services under Section 5 of this Act.

(5) Section 151.359 (Data Center Exemption) is repealed. Industry-specific data center tax exemptions are NAICS-code and industry-sector carve-outs prohibited by Section 1-p(h), Article VIII, Texas Constitution.

(6) Section 151.3595 (Large Data Center Projects Exemption) is repealed for the same reasons as Section 151.359.

(b) The following sections of Chapter 151, Texas Tax Code, are not repealed by this Act and remain in full force and effect:

(1) Section 151.309 (Governmental Entities) — exemptions for purchases by governmental entities are retained subject to review in companion TPTRP implementation legislation;

(2) Section 151.307 (Exemptions Required by Prevailing Law) — retained to the extent it preserves exemptions required by the United States Constitution or federal law, specifically including the Internet access service exclusion required by the Internet Tax Freedom Act; and

(3) Section 151.310 (Religious, Educational, and Public Service Organizations) — retained pending review in companion TPTRP implementation legislation addressing TLES scope and First Amendment considerations.

(c) All other exemptions and partial exemptions in Chapter 151, Subchapter H, Texas Tax Code, that are not expressly retained by Subsection (b) of this section and that apply to categories of goods or services that are taxable transactions under Section 5 of this Act are suspended effective upon the taking effect of this Act, pending comprehensive review and conforming amendment in the full TPTRP implementation legislation. The Comptroller shall publish a list of all suspended exemptions not later than 30 days after the effective date of this Act.

SECTION 6. AMENDMENT TO TEXAS BUSINESS ORGANIZATIONS CODE — SOS REGISTRATION PREREQUISITE.

(a) Chapter 9, Texas Business Organizations Code, is amended by adding Subchapter [Z] to read as follows:

SUBCHAPTER [Z]. REGISTRATION PREREQUISITE FOR REMOTE SELLERS UNDER THE UNIFIED TRANSACTION TAX

Sec. 9.[Z].001. APPLICABILITY. This subchapter applies to any out-of-state entity or foreign entity that makes taxable transactions with Texas customers and meets the economic nexus threshold established by Section 151.008(c), Texas Tax Code, or that voluntarily elects to register with this state.

Sec. 9.[Z].002. REGISTRATION REQUIRED BEFORE TRANSACTING BUSINESS. An out-of-state entity or foreign entity subject to this subchapter may not transact business with Texas customers unless the entity holds a current SOS Authorization issued by the Secretary of State under this subchapter.

Sec. 9.[Z].003. COORDINATED REGISTRATION PROCESS. The Secretary of State and the Comptroller shall establish and maintain a coordinated single-filing process through the Portal through which an out-of-state or foreign entity may simultaneously apply for SOS Authorization and a Texas Tax Registration Certificate from the Comptroller. The coordinated process shall issue both authorizations upon a single completed application.

Sec. 9.[Z].004. CONTRACT UNENFORCEABILITY. An out-of-state entity or foreign entity that transacts business with Texas customers without a current SOS Authorization may not maintain an action, suit, or proceeding in any court of this state arising out of or related to any transaction conducted without the required authorization.

Sec. 9.[Z].005. EQUAL TREATMENT. The SOS Authorization requirements of this subchapter apply to out-of-state and foreign entities on the same terms as registration requirements applicable to Texas-domiciled businesses. No out-of-state or foreign entity may receive more favorable or less favorable registration terms than a Texas-domiciled business based on its domicile.

SECTION 7. TEXAS FOREIGN ENTITY TRANSACTION TAX PORTAL.

(a) The Comptroller shall establish, operate, and maintain the Texas Foreign Entity Transaction Tax Portal — an online-only compliance system through which remote sellers and foreign entities may register for, file, and remit Unified Transaction Tax obligations.

(b) The Portal shall provide:

(1) online registration for remote sellers, including foreign entities domiciled outside the United States, without requiring a United States Social Security Number or Individual Taxpayer Identification Number as a mandatory condition of registration; the Portal shall accept a foreign entity's home-country tax identification number or a Texas Comptroller Foreign Entity Tax Identification Number issued to entities without a home-country number;

(2) issuance of a Texas Tax Registration Certificate upon completion of registration and confirmation of SOS Authorization;

(3) a rate lookup tool allowing a registrant to determine the applicable Unified Transaction Tax rate by customer location, updated to reflect any legislative rate adjustment;

(4) a consolidated quarterly filing system enabling submission of a single return covering all Texas taxable transactions for the reporting period, with separate line items for excluded transactions (Definition Filter) and TLES-exempt transactions reported at $0;

(5) acceptance of payment by ACH electronic funds transfer, international wire transfer, and such other electronic payment methods as the Comptroller may designate by rule;

(6) user interface support in English and Spanish at minimum, with Mandarin Chinese, Hindi, Portuguese, and Filipino added within 18 months of the Portal's initial launch;

(7) a secure account management interface for viewing filing history, permit status, and Comptroller correspondence; and

(8) a voluntary disclosure filing module consistent with Section 13 of this Act.

(c) The Comptroller shall publish and maintain a Public Foreign Entity Registry — a publicly searchable database of all remote sellers and foreign entities holding a current Texas Tax Registration Certificate and a current SOS Authorization. The registry shall be accessible online without charge and updated in real time.