Ending Property Taxes - Retaining Home Rule for Cities Satisfied

Home Rule and the Constitutional Path to Ending Property Taxes in Texas

Why Texas’s Home Rule Doctrine Does Not Block Property Tax Abolition — And Why the Rest of the Plan Can Start Immediately

The Concern This Article Addresses

If you follow the debate over ending property taxes in Texas, you have almost certainly encountered some version of this claim: “Home rule cities have a constitutional right to levy property taxes. The Legislature cannot take that away. The plan is legally impossible.”

This argument comes from city lobbyists, municipal attorneys, and commenters on social media alike. The Texas Municipal League has stated it will “vigorously oppose any legislation that would erode the authority of Texas cities to govern their own local affairs” (Texas Municipal League, 2025). Online, skeptics invoke home rule as proof that property tax elimination is a constitutional dead end.

This article addresses that argument head-on. The Home Rule doctrine is real, legally grounded, and must be taken seriously. But it is an argument about the wrong legal vehicle — it applies to statutes, not to constitutional amendments. The proven constitutional amendment path bypasses every Home Rule objection entirely.

Critically, there is a distinction that too many people miss: the flat sales tax plan can start immediately by statute. Ending the franchise tax, restructuring sales taxes, delivering revenue relief to Texans — all of this is purely statutory and requires no constitutional amendment. Only the final step — the actual prohibition on local governments levying property taxes — requires a constitutional amendment. That is not a flaw in the plan. That is the system working exactly as designed.

Part I: What Is Home Rule in Texas?

Texas originally governed all its cities under Dillon’s Rule — a legal doctrine holding that municipalities possess only those powers expressly granted by the state legislature (Public Health Law Center, 2020). Under Dillon’s Rule, cities are creatures of the state with no inherent authority; they can do only what the Legislature specifically permits.

In 1912, Texas voters changed that by amending the state constitution. Article XI, Section 5 now grants cities with populations exceeding 5,000 the right to adopt their own charters and exercise broad self-governance (Texas Constitution, Art. XI, §5). Today, more than 370 Texas cities operate under home rule charters, including every major city in the state — Houston, Dallas, San Antonio, Fort Worth, Austin, and El Paso (Texas Municipal League, n.d.).

Home rule cities derive their powers not from legislative permission but from the Texas Constitution itself. The Texas Supreme Court affirmed this in Proctor v. Andrews, holding that under Article XI, Section 5, “the power of the city to act is as broad as the power of the state to act” (Proctor v. Andrews, 972 S.W.2d 729, 733 [Tex. 1998]). When the Legislature seeks to limit home rule authority, it must express that intent with “unmistakable clarity” (Dallas Merchants & Concessionaire’s Ass’n v. City of Dallas, 852 S.W.2d 489, 491 [Tex. 1993]).

Key Constitutional Text — Article XI, §5: “Said cities may levy, assess and collect such taxes as may be authorized by law or by their charters; but no tax for any purpose shall ever be lawful for any one year, which shall exceed two and one-half per cent. of the taxable property of such city.”

Note the dual source of taxing authority: “authorized by law or by their charters.” This constitutional grant is what distinguishes home rule taxing power from a mere statutory privilege.

This matters because it means the Legislature’s power over home rule cities is one of limitation, not creation. General law cities (those under 5,000 population or those that have not adopted charters) rely entirely on legislative grants of power. Home rule cities do not. Their taxing authority has a constitutional floor that ordinary legislation cannot reach.

Part II: The Arguments Opponents Raise

Understanding the Home Rule doctrine is important because it gives structure to several recurring arguments against property tax elimination. Here are the six most common, drawn from public discourse, municipal advocacy, and legislative debate.

Argument 1: “The Legislature Can’t Strip Constitutional Taxing Power by Statute”

This is the strongest form of the Home Rule argument and it is largely correct as stated. Because home rule cities draw taxing authority from Article XI, §5 — not from a legislative grant — a simple statute saying “cities may no longer levy property taxes” would face serious constitutional challenge. The HB 2127 (“Death Star”) litigation illustrates this: Houston argued that the bill “is thus antithetical to constitutional home rule and the Texas Constitution” (City of Houston, 2023). Even the HB 2127 text itself carved out taxation from its preemption provisions, suggesting the Legislature recognized that stripping taxing authority requires a different constitutional mechanism (HB 2127, §4[1]).

Argument 2: “Home Rule Cities Will Sue”

Houston, San Antonio, and El Paso have already demonstrated willingness to litigate state preemption, filing suit against HB 2127 in 2023 (Texas Tribune, 2023). Monty Wynn of the Texas Municipal League warned that legislative constraints would “financially handcuff Texas cities from serving their residents” (Governing, 2025). This argument is credible — if the vehicle chosen is a statute. It is irrelevant if the vehicle is a constitutional amendment.

Argument 3: “Cities Would Need to Change Their Own Charters”

Because home rule charters include taxing provisions authorized by Article XI, §5, and because charter amendments require voter elections and can occur no more than once every two years, some argue that property tax elimination would require hundreds of individual charter amendment elections (Texas Constitution, Art. XI, §5). This argument applies only if the change is pursued through statute. A constitutional amendment supersedes charter provisions directly — no city-by-city action is required.

Argument 4: “This Destroys Local Control”

This is the most emotionally resonant objection. The Texas AFT has argued that “shifting from local property taxes to increased state-level funding would also result in a loss of local control over schools and other community services” (Texas AFT, 2024). On Reddit, one highly upvoted comment warned that “Independent School Districts would depend entirely on state funding” with “numerous questionable conditions, ultimately undermining the autonomy of these self-governing school districts” (u/jeremysbrain, r/texas, 2026). This concern deserves a full answer, which Part V provides.

Argument 5: “Sales Tax Replacement Creates State Dependency”

The Texas Taxpayers and Research Association found that “if local property tax were replaced by state sales tax, a mechanism to distribute state funds to counties, cities, and other local governments would need to be developed” (TTARA, 2024). Lt. Gov. Dan Patrick has warned that full elimination “could require a significant increase in the state sales tax to replace the lost revenue” (Texas Standard, 2025). These are fiscal design questions, not constitutional barriers, and the flat sales tax plan addresses them through dedicated local revenue streams.

Argument 6: “Bond Obligations Make This Impossible”

Texas local governments carry over $330 billion in outstanding debt, with general-obligation bonds directly backed by property taxes (Texans for Fiscal Responsibility, 2025). The Texas Constitution itself requires that “no debt shall ever be created by any city, unless at the same time provision be made to assess and collect annually a sufficient sum to pay the interest thereon” (Texas Constitution, Art. XI, §5). This is a legitimate implementation concern that requires a transition mechanism. Education Code §45.001 governs school district bond authority, and any elimination plan must include a structured process for transitioning bond obligations from property-tax-backed revenue to the new sales-tax-based revenue streams. The 5% flat sales tax plan acknowledges this need and accounts for it within the dedicated local revenue allocation.

| Argument | Core Claim | Valid Against Statute? | Valid Against Amendment? |

|---|---|---|---|

| Can’t strip constitutional power | Art. XI, §5 grants taxing authority | Yes | No |

| Cities will sue | Litigation will follow | Yes | No |

| Charter amendments needed | Each city must amend charter | Partially | No |

| Destroys local control | Cities lose self-governance | Policy concern | Policy concern — addressed by plan |

| Sales tax creates dependency | Cities become dependent on state | Design question | Design question — addressed by plan |

| Bond obligations | Debt service requires property tax | Must be addressed | Must be addressed — transition mechanism required |

Sources: Texas Constitution, Art. XI, §5; Proctor v. Andrews (1998); Dallas Merchants (1993); TTARA (2024); TML Legislative Program (2025); Education Code §45.001.

Part III: The Constitutional Amendment Path — Proven and Available

Every one of the legal arguments above collapses when the vehicle chosen is a constitutional amendment rather than a statute. Article XVII, Section 1 of the Texas Constitution provides the mechanism (Texas Constitution, Art. XVII, §1). A constitutional amendment:

- Overrides all inconsistent provisions, including Article XI, §5’s charter-based taxing authority

- Cannot be challenged on Home Rule grounds, because an amendment is the Constitution

- Permanently resolves litigation risk from home rule cities

- Follows exact precedent used to abolish state-level ad valorem taxes in 1968

| Step | Requirement | Details |

|---|---|---|

| 1. Joint Resolution | Introduced in House or Senate | HJR 32 already drafted by Rep. Muñoz (89th Legislature) |

| 2. Legislative Approval | Two-thirds of all members of both chambers | 100 House votes, 21 Senate votes required |

| 3. Voter Ratification | Simple majority at statewide election | Typically held November of odd-numbered years |

| 4. Implementation | Companion statute activates | HB 260 was drafted as implementing legislation |

Sources: Texas Constitution, Art. XVII, §1; HJR 32, 89th Legislature, 1st Called Session; HB 260, 89th Legislature.

Is this achievable? The historical record says yes. Texas has passed 530 constitutional amendments out of 714 proposed since 1876 — a voter approval rate of approximately 74.5% (Texas State Historical Association, n.d.). In the November 2025 election alone, voters approved all 17 proposed amendments, including five property-tax-related measures that passed with between 65% and 89% support (Texas Policy Research, 2025). The political appetite for property tax reform through constitutional amendment is not theoretical; it is demonstrated.

The 1968 Precedent: Texas already abolished an entire category of property taxes through constitutional amendment. Article VIII, Section 1-e, approved by voters on November 5, 1968, eliminated all state-level ad valorem taxes with the declaration: “No State ad valorem taxes shall be levied upon any property within this State” (Texas Constitution, Art. VIII, §1-e). The 1968 amendment used a phased schedule — reducing school property tax rates from $0.35/$100 by $0.05 annually to zero by 1975 — mirroring the type of phased approach that would be appropriate for local property tax elimination (Texas Comptroller, 2015).

HJR 32, filed during the 89th Legislature’s 1st Called Special Session, proposes adding Subsection (b-1) to Article VIII, Section 1: “A political subdivision of this state may not impose an ad valorem tax on real or personal property in this state for any purpose on or after January 1, 2031” (HJR 32, 89th Legislature). Its companion bill, HB 260, explicitly states it “has no effect” unless the constitutional amendment is approved by voters — the definitive legislative acknowledgment that abolition requires the constitutional path (HB 260, 89th Legislature).

Part IV: What Can Be Done Now — Without Any Amendment

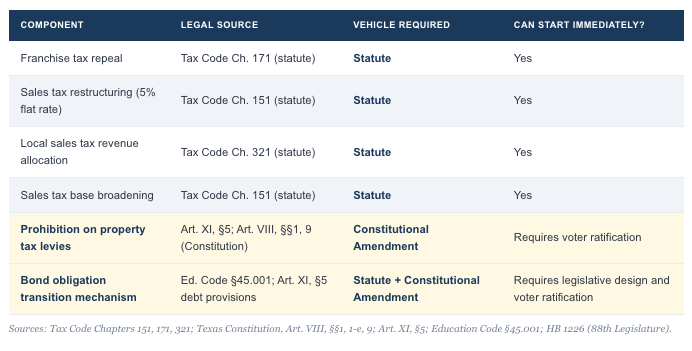

This is the most important section of this article. The debate about Home Rule and constitutional amendments, while legally significant, obscures a critical fact: the majority of the flat sales tax plan does not require a constitutional amendment at all.

The Texas franchise tax is codified at Tax Code, Chapter 171. It is entirely statutory. The Texas Constitution does not require the Legislature to maintain a franchise tax. Multiple bills to repeal it outright have been introduced, including HB 1226 during the 88th Legislature, which simply stated “Chapter 171, Tax Code, is repealed” — with no constitutional amendment companion (HB 1226, 88th Legislature). The Legislature can eliminate the franchise tax tomorrow by a simple majority vote.

The state sales tax is codified at Tax Code, Chapter 151. It is also entirely statutory. The current 6.25% state rate was set by statute and has been modified by statute multiple times. There is no constitutional cap on sales tax rates in Texas (Texas Constitution, Art. VIII). The Legislature can raise, lower, restructure, or broaden the sales tax base by passing a bill.

This means the proposed 5% flat sales tax structure — with 0.75% dedicated to the state, 0.75% to counties, and 3.5% to cities, school districts, and special districts — can be implemented by statute. The revenue relief begins immediately. The franchise tax can be repealed immediately. The new revenue architecture can be built immediately.

| Component | Legal Source | Vehicle Required | Can Start Immediately? |

|---|---|---|---|

| Franchise tax repeal | Tax Code Ch. 171 (statute) | Statute | Yes |

| Sales tax restructuring (5% flat rate) | Tax Code Ch. 151 (statute) | Statute | Yes |

| Local sales tax revenue allocation | Tax Code Ch. 321 (statute) | Statute | Yes |

| Sales tax base broadening | Tax Code Ch. 151 (statute) | Statute | Yes |

| Prohibition on property tax levies | Art. XI, §5; Art. VIII, §§1, 9 (Constitution) | Constitutional Amendment | Requires voter ratification |

| Bond obligation transition mechanism | Ed. Code §45.001; Art. XI, §5 debt provisions | Statute + Constitutional Amendment | Requires legislative design and voter ratification |

Sources: Tax Code Chapters 151, 171, 321; Texas Constitution, Art. VIII, §§1, 1-e, 9; Art. XI, §5; Education Code §45.001; HB 1226 (88th Legislature).

The two-track approach is straightforward: statutes for immediate relief, amendment for permanent elimination. Texans do not need to wait for a constitutional amendment election to begin seeing the benefits of tax reform. The Legislature can act in its next session to restructure the sales tax, eliminate the franchise tax, and build the revenue distribution infrastructure — while simultaneously sending a constitutional amendment to the voters for the final step of prohibiting property tax levies.

Part V: The “Local Control” Question — Answered

The local control concern deserves more than a dismissal. It deserves a direct answer.

First, the legal reality: home rule self-governance does not mean immunity from constitutional change. Cities are political subdivisions of the state of Texas, not sovereign entities. The Texas Supreme Court has confirmed that home rule authority is “as broad as the power of the state to act” (Proctor v. Andrews, 1998) — but that formulation means state constitutional authority, exercised through amendment, supersedes city authority. As legal expert Dan Erben noted regarding preemption litigation, “cities and counties are creations of the state. For them to say ‘this is unconstitutional’ — that would be a hard case to prove because the state would come back and say ‘you don’t exist but for us’” (Daily Texan, 2025).

Second, the plan preserves local control where it matters most. Under the proposed structure, cities set their own sales tax rate within the 3.5% cap. The Texas Comptroller already collects and distributes local sales taxes — this is not a new mechanism but an expansion of existing infrastructure. Cities retain full authority over spending decisions, zoning, annexation, local services, ordinances, and governance structure. What changes is the revenue source, not the decision-making authority.

Third, the current property tax system actually undermines democratic accountability in ways its defenders rarely acknowledge. Unelected appraisal districts determine property values. Appraisal-driven tax increases happen without any elected official casting a vote. Property owners face annual uncertainty over assessments they cannot predict and often cannot effectively challenge. A sales-tax-funded system ties revenue directly to economic activity that is transparent and predictable — and rate changes require affirmative legislative action.

Local control is exercised through spending decisions, not exclusively through taxing decisions. A city that receives a predictable revenue stream from sales taxes retains every bit as much local governance authority as one that receives revenue from property taxes. The difference is that property owners are no longer taxed on the mere act of owning their home.

Part VI: Bond Obligations — Solved, Not Ignored

Opponents of property tax elimination often point to $330.9 billion in outstanding local government debt as a dealbreaker (Texans for Fiscal Responsibility, 2025; Texas Bond Review Board, 2024). The argument goes: because general obligation bonds are pledged to ad valorem taxes, eliminating property taxes would trigger a catastrophic default on hundreds of billions in debt.

This concern deserves a serious answer. Here it is.

The Fiscal Reality: The Money Is Already There

The $330.9 billion figure represents total outstanding principal — not the annual payment due. Annual debt service across all Texas local governments is approximately $20–25 billion per year, with school districts accounting for $11.6 billion of that total (TTARA, 2025; TASBO, 2024). The 5% flat sales tax plan replaces 100% of the $86.6 billion property tax levy — which already includes every dollar of bond debt service currently being paid. Under the plan’s local 3.50% tier, $121.4 billion flows to local entities annually, against $111.1 billion in total local needs including debt service. The bonds are fiscally covered with a $10.3 billion surplus.

This is not a money problem. It is a legal covenant problem.

The Legal Covenant Issue

Texas GO bonds contain an explicit contractual pledge to “levy, pledge, assess, and collect annual ad valorem taxes sufficient to pay the principal of and interest on the bonds” (Texas Education Code §45.001(a)(2)). The Texas Municipal League confirms that “general obligation bonds are secured by a pledge of city property taxes” and that “general revenue sales tax generally cannot be pledged to pay off bonds” (TML Revenue Manual, 2023). The U.S. Supreme Court’s Contract Clause jurisprudence (United States Trust Co. v. New Jersey, 1977) applies heightened scrutiny when a state impairs its own bond contracts. And the Texas Permanent School Fund currently guarantees approximately $121 billion in school district bonds — a guarantee that requires bonds to be “backed by a property tax levy” (Texas PSF, 2025).

The question, then, is not whether the revenue exists to pay the bonds. It does. The question is how to satisfy the legal covenant while eliminating property taxes. Five approaches have been proposed or implemented in various jurisdictions:

Option 1: I&S Carve-Out (The “Michigan Model”)

Eliminate all maintenance and operations (M&O) property taxes immediately. Retain a narrow Interest & Sinking (I&S) levy only for pre-existing voter-approved bonds, which sunsets automatically as each bond matures over approximately 30 years. Michigan’s Proposal A (1994) did exactly this — eliminating school M&O property taxes and replacing them with sales tax revenue while leaving I&S levies untouched (Citizens Research Council of Michigan, 2018). California’s Proposition 13 (1978) carved out pre-existing voter-approved bonds from the 1% property tax cap (California Constitution, Art. XIII A, §1(b)). Colorado’s SB 233 (2024) excluded bonded-debt revenue from new property tax caps.

Strength: Lowest legal risk — no contract impairment because the pledged tax continues for its contractual purpose. Weakness: Property taxes don’t go to true zero on day one; homeowners still pay a declining I&S levy (roughly 13% of the current school district levy) that phases out over time.

Option 2: State Revenue Replacement Grants

The state uses a portion of the new sales tax revenue to make bond debt service payments on behalf of local governments through a dedicated fund. Kansas’s Property Tax Freedom Act (SB 488, 2026) provides the most detailed contemporary template: a “Property Tax Freedom Reserve Fund” receives a portion of the replacement consumption tax, and the State Treasurer disburses grants equal to each locality’s full GO bond debt service (Kansas Legislature, 2026). Michigan operates a School Bond Loan Fund as a smaller-scale version (Citizens Research Council of Michigan, 2018).

Strength: Property taxes go to true zero immediately; bondholders receive guaranteed payments from a constitutionally dedicated fund. Weakness: Requires ~$20–25 billion in annual state appropriation; future legislatures could theoretically defund a statutory (non-constitutional) program.

Option 3: Direct Revenue Substitution

Because the plan replaces 100% of property tax revenue with an equal or larger sales tax allocation to the same local entities, those entities continue making bond payments from their new revenue stream. The constitutional amendment would explicitly declare sales tax revenue as the successor obligation with equal legal standing.

Strength: Simplest implementation; requires no separate fund or carve-out. Weakness: Untested — no state has attempted full revenue substitution without a carve-out or guarantee. Bondholders could argue the specific ad valorem pledge was impaired regardless of payment continuity. The Kansas tax experiment (2012) showed that even partial revenue disruption increased local borrowing costs by 34 basis points and reduced high-rating probabilities by 9.1 percentage points (Baruch CUNY, 2021).

Option 4: Mass Refunding

Issue new sales-tax-backed bonds to retire all existing property-tax-backed GO bonds. The old bonds get paid off; the new bonds carry a sales tax pledge. This is standard municipal practice for individual bond issues, but has never been attempted at the $229 billion scale of Texas GO debt.

Strength: Cleanly replaces the legal pledge on each bond. Weakness: The 2017 Tax Cuts and Jobs Act eliminated advance refunding of tax-exempt bonds with new tax-exempt bonds (MRSC, 2025). Many bonds are not yet callable. Transaction costs at this scale would run into billions. This would be the largest municipal bond refinancing in U.S. history.

Option 5: The Recommended Approach — Immediate Elimination with Constitutional Guarantee

Recommended: The constitutional amendment prohibits all new property tax levies. For existing bond obligations, the amendment provides dual protection: (1) local entities continue making I&S payments from their new sales tax allocation, which exceeds their prior property tax revenue; and (2) the state constitutionally guarantees full debt service from the Rainy Day Fund allocation ($5.7 billion annually under the plan) if any shortfall occurs. No new GO bonds may be backed by property taxes from the effective date forward. The guarantee automatically terminates when the last pre-existing bond matures.

This approach draws on the strongest elements of every precedent:

- From California (Prop 13): The principle that a constitutional amendment can restructure the tax system without impairing existing bond contracts, provided adequate protection is built in (California AG Opinion No. 79-424, 1979).

- From Michigan (Proposal A): The demonstrated success of replacing property tax revenue with sales tax revenue for school operations while maintaining bond security (Citizens Research Council of Michigan, 2018).

- From Kansas (SB 488): The revenue replacement grant mechanism funded by the new consumption tax (Kansas Legislature, 2026).

- From the plan itself: The $5.7 billion annual Rainy Day Fund allocation from the state’s 0.75% tier provides a constitutionally dedicated backstop. The $10.3 billion local surplus provides additional margin.

Under this approach, property taxes go to true zero for every homeowner on day one. Bondholders are protected by a constitutional guarantee backed by the full faith and credit of the state of Texas. The guarantee self-liquidates over approximately 30 years as pre-existing bonds mature. And the fiscal math works: annual debt service of $20–25 billion is a fraction of the $121.4 billion flowing through the local tier.

| Approach | Property Tax on Day 1 | Legal Risk | Bondholder Protection | Precedent |

|---|---|---|---|---|

| 1. I&S Carve-Out | Reduced ~87% (M&O eliminated; I&S remains) | Very low | Ad valorem pledge preserved for existing bonds | Michigan Proposal A; California Prop 13; Colorado SB 233 |

| 2. State Revenue Grants | Eliminated (true zero) | Low | State pays debt service from dedicated fund | Kansas SB 488; Michigan School Bond Loan Fund |

| 3. Direct Revenue Substitution | Eliminated (true zero) | Moderate–high | Payments continue from new revenue; no formal guarantee | No direct precedent at scale |

| 4. Mass Refunding | Eliminated (true zero) | Low per bond; high at scale | Old bonds retired; new bonds carry sales tax pledge | Standard practice; never at $229B scale |

| 5. Immediate Elimination + Constitutional Guarantee (Recommended) | Eliminated (true zero) | Low | Sales tax allocation + state Rainy Day Fund backstop | Combines CA, MI, KS precedents |

Sources: California Constitution, Art. XIII A, §1(b); California AG Opinion No. 79-424 (1979); Citizens Research Council of Michigan (2018); Kansas SB 488 (2026); Baruch CUNY (2021); Texas Bond Review Board (2024); TTARA (2025); U.S. Trust Co. v. New Jersey, 431 U.S. 1 (1977).

What Happens to Municipal Bonds Going Forward?

Under the plan, no new general obligation bonds may be backed by property taxes from the effective date of the constitutional amendment. This raises a natural question: how do local governments finance capital projects — new schools, roads, water infrastructure — without property-tax-backed bonds?

The answer is sales-tax revenue bonds, which are already a well-established instrument in the municipal bond market. Nuveen, one of the nation’s largest municipal bond managers, has documented that sales tax revenue bonds “have grown significantly over the past two decades” and that consumer spending “powers municipal infrastructure” through dedicated sales tax pledges (Nuveen, 2025). Key advantages of sales-tax-backed bonds in Texas under the plan:

- Broad, stable tax base: The 5% flat tax on the full $3,468.3 billion gross sales base is far broader and more diversified than any single jurisdiction’s property tax base. Economic diversification reduces single-sector risk.

- Voter accountability: New bond issuance would require voter approval with a dedicated local sales tax surcharge, tying capital spending directly to democratic consent — exactly as property tax bonds do today, but without taxing the act of homeownership.

- Existing infrastructure: The Texas Comptroller already collects and distributes local sales taxes. No new collection mechanism is needed (Texas Comptroller, 2025).

- Rating agency treatment: Sales tax revenue bonds are routinely rated at investment grade. The broader tax base and state constitutional dedication of revenue could actually support stronger credit ratings than property-tax-backed bonds from smaller taxing districts with concentrated tax bases.

- Federal tax exemption preserved: The 2025 One Big Beautiful Bill Act preserved the federal tax exemption for all municipal bonds, including both governmental purpose and private activity bonds (Jackson Walker, 2025). New sales-tax-backed bonds would retain the same tax-exempt status as current GO bonds.

Texas already has a successful model for this. The state’s existing local sales tax system (Tax Code Chapter 321) distributes billions annually to cities and special districts. Ogden City, Utah demonstrated that sales tax revenue can be irrevocably pledged to bond obligations through interlocal agreements (Ogden City Council, 2023). The transition simply shifts the pledge from one tax instrument to another — from a tax on ownership to a tax on consumption — while maintaining the same bondholder protections and the same investor confidence.

The elimination of property taxes does not end municipal borrowing. It modernizes it.

Opening Municipal Bonds to Every Texan

The transition to sales-tax revenue bonds creates more than a new funding mechanism. It creates a once-in-a-generation opportunity to redesign who gets to invest in Texas’s public infrastructure — and who earns the returns.

Today, Texas property owners pay the taxes that service approximately $552 billion in local government debt (Texas Public Policy Foundation, 2026). Yet the investment returns on those bonds flow overwhelmingly to institutional investors, mutual funds, and wealthy out-of-state bondholders. Retail investors hold roughly 44.5% of the $4.4 trillion national municipal bond market, but they face structural barriers that effectively exclude ordinary families: $5,000 minimum denominations, opaque over-the-counter pricing, and broker-dealer markups averaging 0.55% more than institutional buyers pay for the same bonds (S&P Global, 2022; MSRB, 2022). The average Texan who votes to approve a school bond cannot afford to invest in it.

This is not a theoretical proposal. Cities across the country have already demonstrated that citizens will invest directly in their communities when given the chance:

- Denver, Colorado has sold “mini-bonds” five times since 1990 — the most recent in 2014, when $12 million in bonds at $500 minimums sold out in under one hour to approximately 1,000 Colorado residents. The bonds funded parks, roads, libraries, and community health facilities (City and County of Denver, 2014).

- Cambridge, Massachusetts issued $2 million in mini-bonds in 2017 at $1,000 minimums and a 1.6% tax-free rate, funding school improvements and street reconstruction. Cambridge carries a AAA rating from all three major agencies (Cambridge Day, 2017).

- Madison, Wisconsin sold $2.1 million in community bonds in 2018 at $500 minimums, prioritizing city residents first, then county, then national buyers (AP News, 2018).

- United Kingdom: The Community Municipal Investments program, administered through the Abundance Investment platform, has raised £21.3 million from 18 local councils with investment minimums as low as £5 — the most mature citizen bond model operating today (Abundance Investment, 2025).

- U.S. Treasury: The federal government already sells bonds directly to citizens through TreasuryDirect at minimums of just $25 — no broker, no markup, no middleman (U.S. Department of the Treasury, n.d.).

Five approaches exist for implementing citizen bond investment in Texas, ranging from immediately actionable to long-term transformative:

| Approach | Mechanism | Min. Investment | Timeline | Precedent |

|---|---|---|---|---|

| 1. Texas Mini-Bond Program | Require a “citizen tranche” on all new bond issuances sold directly to residents | $100–$500 | Immediate | Denver, Cambridge, Madison |

| 2. Texas Bond Direct | Centralized state platform (modeled on TreasuryDirect) for all Texas municipal bonds | $100 | 18–24 months | TreasuryDirect |

| 3. Tokenized Bonds | Blockchain-based fractional ownership enabling micro-investments | $10–$50 | 3–5 years | Berkeley CA; SEC sandbox (2025) |

| 4. Texas Family Fund | Automatic municipal bond allocation within each family’s state-managed fund | Automatic | 24–36 months | Alaska Permanent Fund; Baby Bonds |

| 5. Hybrid Model (Recommended) | Phased combination: citizen tranches → state platform → tokenization, with Family Fund as parallel vehicle | $100 → $10 | Phased | Combines all above |

Sources: City and County of Denver (2014); Cambridge Day (2017); AP News (2018); Abundance Investment (2025); U.S. Dept. of Treasury (n.d.); SEC (2025); MSRB (2016).

Phase 1 (Immediate): State legislation requiring citizen tranches on all new Texas municipal bond issuances. MSRB Rule G-11 already permits issuers to establish retail order periods with geographic priority — municipalities can begin prioritizing resident purchases under existing federal rules with minimal new regulation (MSRB, 2016).

Phase 2 (18–24 months): Build and launch the Texas Bond Direct platform through the State Comptroller’s office, which already collects and distributes local sales taxes statewide. This creates a centralized marketplace where any Texan can browse and invest in any Texas municipal bond from $100.

Phase 3 (3–5 years): Integrate tokenization capabilities as the SEC regulatory sandbox matures, reducing minimums toward $10–$50.

Ongoing: The Texas Family Fund serves as an additional entry point for families who prefer passive, automatic, diversified municipal bond exposure.

The legal path is clear. Municipal bonds are exempt from SEC registration under the Tower Amendments of 1975, meaning government issuers can sell directly to citizens without a registered dealer if state law enables it (Securities Act of 1933, §3(a)(2)). The 2025 One Big Beautiful Bill Act preserved the federal tax exemption for all municipal bonds — new sales-tax-backed bonds held by citizen investors would carry the same tax-exempt returns as any institutional holding (Jackson Walker, 2025). Current long-term municipal bond yields of 4.5–5.0% tax-free translate to taxable equivalents of 7.5–9.0% for investors in the 35% bracket (PIMCO, 2025) — far exceeding savings accounts, CDs, or Treasury bills.

The civic case is equally strong. When citizens own their community’s bonds, coupon payments stay local rather than flowing to out-of-state institutions. Citizen bondholders become financially invested monitors of fiscal management, strengthening democratic accountability. Research from the UK’s Community Municipal Investments program found that citizen bond ownership “improve[s] attitudes towards the council” and provides “a simple and low-risk way to connect the financial and non-financial ambitions of local residents” (Bauman Institute, 2024). The Roosevelt Institute has identified the current municipal bond structure as contributing to wealth inequality — working-class taxpayers service bonds owned by upper-income investors (Roosevelt Institute, 2023). A citizen-direct program inverts that arrangement.

The elimination of property taxes does not merely modernize how Texas borrows. It opens the door to a system where every Texan who helps fund public infrastructure through their daily purchases can also earn a return on that investment — a guaranteed, tax-advantaged return backed by the full faith and credit of their own community.

Conclusion: The Question Is Not If — It’s When

The Home Rule doctrine is real and legally grounded. It must be taken seriously — and this article has taken it seriously, walking through the constitutional text, the case law, and the arguments raised by opponents from the Texas Municipal League to social media commenters to Lieutenant Governor Dan Patrick.

But Home Rule is an argument about the wrong legal vehicle. It applies to statutes. It does not apply to constitutional amendments. A properly drafted and ratified constitutional amendment under Article XVII, Section 1 overrides every inconsistent provision in the Texas Constitution, including Article XI, Section 5’s grant of taxing authority to home rule cities. This is not a novel legal theory. It is how the Texas Constitution has been amended more than 530 times since 1876. It is how the state-level property tax was abolished in 1968. It is how five property-tax-relief amendments were approved by voters in November 2025.

And the bond question — $330.9 billion in outstanding local debt — is answered. The plan’s revenue fully covers annual debt service. The constitutional amendment guarantees bondholder protection through the state’s Rainy Day Fund allocation. The obligation self-liquidates as bonds mature. Going forward, sales-tax revenue bonds replace property-tax-backed bonds with a broader, more stable, and more equitable instrument — and for the first time, every Texan can invest directly in the bonds that build their schools, roads, and infrastructure, earning guaranteed, tax-advantaged returns through a phased citizen investment program.

The rest of the plan — the flat sales tax, the franchise tax elimination, the revenue restructuring — can start immediately by statute. No constitutional amendment required. No Home Rule barrier. No waiting.

77.97% of Republican primary voters have already said they want property taxes eliminated (Republican Party of Texas, 2026). The constitutional mechanism is proven, available, and has already been drafted. The question is not whether we can end property taxes in Texas. The question is when we choose to.

Annotated Bibliography

Texas Constitution, Art. XI, §5. (1912, as amended). Justia Law. https://law.justia.com/constitution/texas/sections/cn001100-000500.html

The Home Rule Amendment itself. Grants cities with populations exceeding 5,000 the constitutional authority to adopt charters, levy taxes, and exercise broad self-governance. The dual “authorized by law or by their charters” language is the foundation of the Home Rule taxing-power argument analyzed throughout this article.

Texas Constitution, Art. VIII, §1-e. (1968, as amended 1982, 2001). Justia Law. https://law.justia.com/constitution/texas/sections/cn000800-01-e00.html

The provision abolishing state-level ad valorem taxes, approved by Texas voters on November 5, 1968. Establishes the direct constitutional precedent that an entire category of property taxes can be eliminated through the amendment process. The phased implementation schedule provides a model for how local property tax elimination could be structured.

Texas Constitution, Art. XVII, §1. (1876). Tarlton Law Library, University of Texas. https://tarlton.law.utexas.edu/constitutions/texas-1876-en/article-17-mode-amending-constitution-state

The constitutional amendment provision. Requires a two-thirds vote of all elected members of both legislative chambers and majority voter ratification. Provides the legal mechanism by which a property tax abolition amendment would override Article XI, Section 5 and all other inconsistent constitutional provisions.

Proctor v. Andrews, 972 S.W.2d 729 (Tex. 1998). https://law.counselstack.com/opinion/proctor-v-andrews-tex-1998

Texas Supreme Court decision establishing that home rule city power under Article XI, Section 5 is “as broad as the power of the state to act.” Also held that home rule cities, as political subdivisions created by the Constitution, lack standing to assert due process rights against laws that govern them. Central to the constitutional analysis of Home Rule taxing authority.

Dallas Merchants & Concessionaire’s Ass’n v. City of Dallas, 852 S.W.2d 489 (Tex. 1993).

The landmark Texas Supreme Court case establishing the “unmistakable clarity” standard for legislative preemption of home rule authority. Held that a home rule city “possesses the full power of self government” and looks to the Legislature “not for grants of power, but only for limitations on their power.” Demonstrates why statutory property tax abolition faces legal risk while the constitutional amendment path does not.

Texas Legislature Online. (2025). HJR 32 — 89th Legislature, 1st Called Session. https://capitol.texas.gov/tlodocs/891/billtext/html/HJ00032I.htm

The proposed constitutional amendment to abolish local ad valorem taxes effective January 1, 2031. Authored by Rep. Muñoz. Provides a legislative template demonstrating that the constitutional amendment path to property tax elimination has already been drafted and introduced in the Texas Legislature.

Texas Legislature Online. (2025). HB 260 — 89th Legislature, 1st Called Session. https://capitol.texas.gov/tlodocs/891/billtext/html/HB00260I.htm

The companion implementation statute to HJR 32. Explicitly states it “has no effect” unless the constitutional amendment is ratified by voters — the Legislature’s own acknowledgment that property tax abolition requires the constitutional path, not statute alone. Creates a joint interim committee to study sales tax replacement mechanisms.

Texas Constitution and Statutes. Tax Code, Chapter 171 — Franchise Tax. https://statutes.capitol.texas.gov/Docs/TX/htm/TX.171.htm

The purely statutory codification of the Texas franchise tax. Because no constitutional provision mandates its existence, the Legislature can repeal it by simple majority vote. Multiple repeal bills have been introduced, confirming the statutory-only status of this tax.

Texas Constitution and Statutes. Tax Code, Chapter 151 — Limited Sales, Excise, and Use Tax. https://statutes.capitol.texas.gov/Docs/TX/htm/TX.151.htm

The statutory basis for the state sales and use tax. The 6.25% state rate was set and has been modified by statute. No constitutional cap on sales tax rates exists in Texas. This chapter’s purely statutory status means the Legislature can restructure the sales tax — including implementing a 5% flat rate — without a constitutional amendment.

Texas Legislature Online. (2023). HB 1226 — 88th Legislature. https://capitol.texas.gov/tlodocs/88R/billtext/html/HB01226I.htm

Bill to repeal the entire franchise tax (Chapter 171, Tax Code). Filed without a constitutional amendment companion, confirming that franchise tax repeal is a purely statutory action requiring no constitutional change.

Republican Party of Texas. (2026, March 19). Resolution to protect homeowners by eliminating property taxes and excessive state spending. https://texasgop.org/resolution-to-protect-homeowners-by-eliminating-property-taxes-and-excessive-state-spending/

Official RPT resolution citing the 77.97% support for property tax elimination among Republican primary voters (March 2024 advisory ballot). Affirms the party’s platform commitment (Plank 75) to “complete phase out of local property taxes.”

Governor Greg Abbott’s Office. (2025, June 16). Governor Abbott signs property tax relief laws in Denton [Press release]. https://gov.texas.gov/news/post/governor-abbott-signs-property-tax-relief-laws-in-denton

Documents the signing of SB 4 (homestead exemption to $140,000), SB 23 (elderly/disabled exemption to $60,000), and HB 9 (business personal property exemption to $125,000). Notably, all three required constitutional amendments for implementation, confirming that even incremental property tax changes require voter ratification when they touch constitutionally defined provisions.

Texas Taxpayers and Research Association. (2024, August). Should we eliminate local property taxes? [PDF]. https://ttara.org/wp-content/uploads/2024/08/Research_Report_Eliminating_Local_Taxes.pdf

Authoritative fiscal analysis of property tax elimination. Found total local property tax levies of $82.1 billion across 4,644 taxing units. Identified the need for a state distribution mechanism if sales taxes replace property taxes. Provides the baseline fiscal data referenced throughout this article.

Baker Institute for Public Policy. (2025, August 1). Testimony to the Texas Senate Finance Committee on property tax elimination [PDF]. https://www.bakerinstitute.org/sites/default/files/2025-08/Tes-CTBP_Diamond-Property%20Tax-08012025.pdf

Dr. Diamond’s macroeconomic modeling of property tax elimination, projecting GDP increases of 0.8%–1.8% and owner-occupied housing value increases of 14%–27%. Assumes a narrow sales tax base; a broadly applied flat sales tax at a lower rate would produce different fiscal dynamics.

Texas Municipal League. (n.d.). Alphabet soup: Types of Texas cities [PDF]. https://www.tml.org/DocumentCenter/View/244/Types-of-Texas-Cities-PDF

Authoritative reference on the differences between general law and home rule cities in Texas. Confirms that home rule cities “possess the full power of self government” while general law cities rely on legislative grants. Documents the approximately 370+ home rule municipalities in the state.

Texas Policy Research. (2025, November 5). All 17 Texas constitutional amendments pass in 2025 election. https://www.texaspolicyresearch.com/all-17-texas-constitutional-amendments-pass-in-2025-election/

Documents the November 2025 election results in which all 17 proposed amendments were approved, bringing the cumulative total of Texas constitutional amendments to 547. Property-tax-related amendments (Propositions 7, 9, 10, 11, and 13) passed with 65%–89% support, demonstrating strong voter willingness to amend the constitution for tax reform.

Texas State Historical Association. (n.d.). Constitutional amendments. Handbook of Texas Online. https://www.tshaonline.org/handbook/entries/constitutional-amendments

Historical reference documenting 530 amendments adopted since 1876 out of 714 proposed, establishing a voter approval rate of approximately 74.5%. Provides the procedural and political context for constitutional change in Texas.

Texas 2036. (2025, October 14). TX constitutional amendment election: What you need to know. https://texas2036.org/posts/tx-constitutional-amendment-election-what-you-need-to-know/

Non-partisan civic organization explainer of the Texas constitutional amendment process under Article XVII, including the joint resolution requirement, two-thirds legislative vote threshold, and voter ratification mechanism.

Texas Tribune. (2023, July 3). Houston sues state in attempt to block new law that erodes cities’ power. https://www.texastribune.org/2023/07/03/houston-texas-lawsuit-local-control/

Reporting on Houston’s lawsuit challenging HB 2127 on Home Rule grounds. The city argued the bill was “antithetical to constitutional home rule and the Texas Constitution.” Demonstrates the legal strategy cities would employ against a statutory (but not constitutional) property tax elimination attempt.

Texans for Fiscal Responsibility. (2025, October 20). Texas bonds, property taxes, and the debt that harms Texans. https://texastaxpayers.com/texas-bonds-property-taxes-and-the-debt-that-harms-texans/

Analysis documenting $330.9 billion in outstanding local government debt backed by property taxes. The $330.9 billion represents total outstanding principal; annual debt service is approximately $20–25 billion, fully covered by the plan’s local revenue allocation.

Texas Bond Review Board. (2025, January). 2024 Local Government Annual Report [PDF]. https://www.brb.texas.gov/wp-content/uploads/2025/01/2024LocalARFinal.pdf

Authoritative data on Texas local government debt: $333.32 billion total outstanding ($229.2 billion GO/tax-supported, $104.1 billion revenue). School districts: $130.1 billion; cities: $47.3 billion; counties: $15.6 billion. Approximately 24.1% of tax-supported principal retires within five years.

Texas Taxpayers and Research Association. (2025, January). School Finance 101 [PDF]. https://ttara.org/wp-content/uploads/2025/01/TTARA_SchoolFinance101_012425.pdf

Confirms $11.6 billion paid for school debt service in the 2023–24 school year. School district I&S levies represent approximately 26.9% of total school district property tax collections. Provides the annual debt service figure central to the bond transition fiscal analysis.

United States Trust Co. v. New Jersey, 431 U.S. 1 (1977). https://supreme.justia.com/cases/federal/us/431/1/

U.S. Supreme Court decision establishing heightened scrutiny for state impairment of its own bond contracts under the Contract Clause (Art. I, §10). Held that retroactive repeal of a bondholder covenant was unconstitutional because less drastic alternatives existed. The recommended approach (Option 5) satisfies this standard by providing a constitutional guarantee that protects bondholders while achieving the public purpose of tax reform.

Citizens Research Council of Michigan. (2018). The unfinished business of Proposal A: Financing school capital projects. https://crcmich.org/the-unfinished-business-of-proposal-a-financing-school-capital-projects

Documents Michigan’s Proposal A (1994), which eliminated school M&O property taxes and replaced them with sales tax revenue while leaving I&S (bond debt service) levies untouched. Bond issuance nearly doubled post-reform. Demonstrates that property tax restructuring can be accomplished without impairing bond obligations.

California Attorney General. (1979, October 16). Opinion No. 79-424: Proposition 13 and pre-existing bond contracts [PDF]. https://boe.ca.gov/proptaxes/pdf/130_0060.pdf

Concluded that California’s Proposition 13 did not constitute a substantial impairment of pre-existing bond contracts because the voter-approved-debt carve-out preserved bondholder security. Establishes the legal principle that a constitutional amendment restructuring property taxes can survive Contract Clause challenge if adequate bondholder protection is included.

Kansas Legislature. (2026). SB 488 — Kansas Property Tax Freedom Act of 2026 [PDF]. https://www.kslegislature.gov/li/b2025_26/measures/documents/sb488_00_0000.pdf

The most detailed contemporary legislative template for property tax elimination with bond protection. Establishes a “Property Tax Freedom Reserve Fund” providing revenue replacement grants equal to full existing GO bond debt service, funded by a new consumption tax. Provides the state-guarantee mechanism adapted in the recommended approach (Option 5).

Baruch College, CUNY — Marxe School of Public and International Affairs. (2021). State tax cuts and debt market outcomes: An empirical analysis [PDF]. https://marxe.baruch.cuny.edu/wp-content/uploads/sites/7/2021/05/STATE-TAX-CUTS-AND-DEBT-MARKET-OUTCOMES.pdf

Empirical study of the Kansas tax cut experiment (2012–2015). Found that large-scale revenue disruption increased local GO bond borrowing costs by 34 basis points and reduced high-credit-rating probability by 9.1 percentage points. Demonstrates the importance of providing bondholder protection when restructuring state tax systems.

Nuveen. (2025). Consumer spending powers municipal infrastructure. https://www.nuveen.com/en-us/insights/municipal-bond-investing/consumer-spending-powers-municipal-infrastructure

Major municipal bond manager’s analysis documenting the growth of sales-tax revenue bonds in the municipal market. Establishes that sales-tax-backed bonds are a well-established, investment-grade instrument suitable for financing municipal infrastructure.

Texas Municipal League. (2023, November). Revenue manual for Texas cities [PDF]. https://www.tml.org/DocumentCenter/View/3989/Revenue-Manual-November-2023

Authoritative reference confirming that Texas GO bonds are “secured by a pledge of city property taxes” and that “general revenue sales tax generally cannot be pledged to pay off bonds.” Documents the legal distinction between ad valorem tax pledges and sales tax revenue that necessitates a structured bond transition mechanism.

Texas Education Code §45.001. Justia Law. https://law.justia.com/codes/texas/education-code/title-2/subtitle-i/chapter-45/subchapter-a/section-45-001/

The statutory authority for school district bond issuance. Explicitly authorizes districts to “levy, pledge, assess, and collect annual ad valorem taxes” for bond repayment. The specific ad valorem pledge language is the source of the bond covenant issue addressed by the recommended transition approach.

City and County of Denver. (2014). Mini bonds program — Investor information. https://denvergov.org/Government/Agencies-Departments-Offices/Agencies-Departments-Offices-Directory/Department-of-Finance/Our-Divisions/Cash-and-Capital-Funding/Investor-Information/Mini-Bonds

Official documentation of Denver’s fifth mini-bond issuance (2014), which sold $12 million in $500-denomination bonds to approximately 1,000 Colorado residents in under one hour. The most frequently cited US precedent for direct citizen investment in municipal bonds.

Cambridge Day. (2017, February 1). Cambridge readies ‘minibond’ offering letting residents invest in city projects. https://www.cambridgeday.com/2017/02/01/cambridge-readies-minibond-offering-letting-residents-invest-in-city-projects/

Coverage of Cambridge’s $2 million mini-bond offering at $1,000 minimums and a 1.6% tax-free rate. The first US city to issue mini-bonds via a technology platform (Neighborly Securities), demonstrating that online citizen bond sales are operationally feasible.

Associated Press. (2018, October 3). Madison begins sale of ‘community bonds’. https://apnews.com/article/business-lifestyle-madison-gardening-2b8bcc86ef944142b8b99abc6cfb1d4f

AP coverage of Madison’s $2.1 million community bond sale at $500 minimums, funding the Olbrich Botanical Gardens expansion. Notable for the geographic priority structure: Madison residents first, Dane County second, national investors third.

Abundance Investment. (2025). Community Municipal Investments. https://www.abundanceinvestment.com/

The UK platform enabling Community Municipal Investments (CMIs) by 18 local councils with investment minimums as low as £5. Has raised £21.3 million from approximately 3,000 citizen investors. The most mature direct-citizen-to-municipal-bond model currently operating globally.

U.S. Department of the Treasury. (n.d.). About US Savings Bonds. TreasuryDirect. https://treasurydirect.gov/savings-bonds/

The federal government’s direct-to-citizen bond platform, with Series I Bonds at $25 minimums and no broker-dealer intermediary. Proves the operational and legal feasibility of government selling bonds directly to citizens at accessible denominations. A model for the proposed Texas Bond Direct platform.

S&P Global. (2022, June). The hidden costs of retail purchases in municipal bonds [PDF]. https://www.spglobal.com/spdji/en/documents/research/research-the-hidden-costs-of-retail-purchases-in-municipal-bonds.pdf

Foundational study documenting that retail municipal bond investors pay an average transaction cost of 0.72% compared to 0.17% for institutional investors — a 0.55% structural disadvantage. On a $100,000 investment held 10 years, this markup gap costs the retail investor approximately $4,160 more than an identical institutional purchase.

Municipal Securities Rulemaking Board. (2022). Trends in municipal securities ownership [PDF]. https://www.msrb.org/sites/default/files/2022-09/MSRB-Brief-Trends-Bond-Ownership.pdf

Documents that retail investors hold approximately 44.5% of the $4.4 trillion municipal bond market, with household direct holdings at $1.779 trillion. Despite holding the plurality of market share, retail buyers face structural disadvantages in pricing, allocation, and transparency.

Municipal Securities Rulemaking Board. (2016). Issuer considerations for reaching the retail investor [PDF]. https://www.msrb.org/sites/default/files/Reaching-Retail-Investor.pdf

Foundational MSRB guidance on Rule G-11 retail order periods, which already permits municipal issuers to establish geographic priority for local residents in bond offerings. Directly applicable to structuring citizen tranches in Texas bond issuances without new federal regulation.

Texas Public Policy Foundation. (2026, January). Texas local government debt soars to $552 billion. https://www.texaspolicy.com/texas-local-government-debt-soars-to-552-billion/

Documents the scale of Texas local government debt at $552 billion as of 2026. The investment returns on this debt flow overwhelmingly to institutional investors rather than the Texas taxpayers who service it. Establishes the equity argument for citizen bond access.

PIMCO. (2025, September). Municipal bond outlook: Compelling value in a shifting rate environment. https://www.pimco.com/en-us/insights/viewpoints/municipal-bonds

Establishes current long-term municipal bond yields at 4.5–5.0% tax-free, translating to taxable equivalents of 7.5–9.0% for investors in the 35% bracket. Supports the argument that citizen bond investors would earn returns significantly exceeding savings accounts, CDs, and Treasury bills.